En la inversión en situaciones especiales, la volatilidad y las tensiones de financiación no son simples obstáculos que superar, sino las condiciones que permiten generar una atractiva rentabilidad.

Ideas principales:

- Gran potencial estructural: el mercado medio europeo continúa ofreciendo numerosas oportunidades de inversión, dadas las limitadas opciones de financiación de estas compañías y la menor competencia entre inversores.

- Un universo de inversión sin precedentes: la lista de oportunidades en seguimiento del equipo de situaciones especiales ya estaba en máximos históricos antes de la guerra de Irán.

- Un elemento de diversificación: nuestra labor de análisis indica que la inversión en situaciones especiales puede mejorar la rentabilidad ajustada al riesgo en distintas construcciones de cartera, gracias a su atractiva rentabilidad absoluta y a su baja correlación con las clases de activos tradicionales.

La inversión en situaciones especiales consiste en identificar compañías que se enfrentan a problemas de financiación o a una situación concreta, y cuya deuda puede estar valorada a niveles demasiado bajos teniendo en cuenta el resultado esperado.

Estas estrategias se ven favorecidas por los episodios de tensión en la refinanciación, por los desajustes forzados o técnicos, por las situaciones complejas, por los déficits de liquidez, por las situaciones relacionadas con acontecimientos concretos y por el aumento de la volatilidad macroeconómica. En un mundo marcado por la creciente ‘inestabilidad’ macroeconómica, el universo de inversión de las situaciones especiales continúa resultando atractivo.

En este artículo, explicamos por qué el mercado medio europeo sigue ofreciendo oportunidades interesantes, por qué nuestra lista de seguimiento es más amplia que nunca y cómo una asignación estratégica a las situaciones especiales puede favorecer las carteras de inversión.

Atractivo del mercado medio europeo

Pensamos que el mercado medio europeo va a continuar ofreciendo oportunidades atractivas a los inversores, fundamentalmente por tres razones:

1. Se trata de un mercado estructuralmente desatendido: las compañías que conforman el mercado medio europeo son aquellas cuyas estructuras de capital incluyen entre 100 y 500 millones de dólares estadounidenses de deuda. Suelen estar menos diversificadas por producto y región, lo que reduce su capacidad de resistencia en episodios de tensión de los mercados. También suelen tener menos acceso a la financiación que las empresas de mayor tamaño, por lo que las que pagan unos tipos de interés elevados por su deuda pueden tener dificultades para refinanciarse en los mercados de capitales. Por lo tanto, dependen en mayor medida de los bancos, que, en los últimos años, han endurecido sus requisitos de concesión de crédito. Este contexto ofrece una oportunidad clara a los inversores en situaciones especiales.

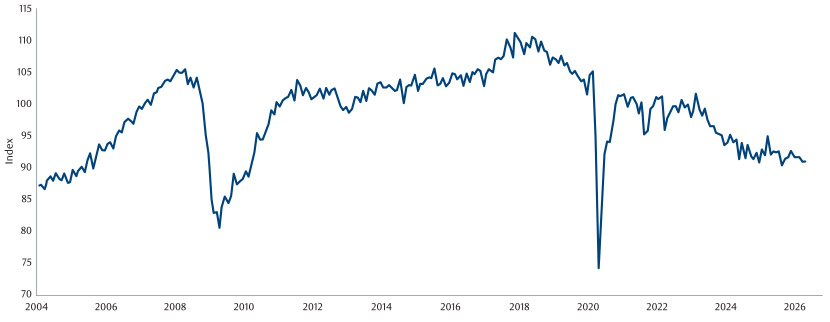

2. La presión cíclica amplía el universo de inversión: el contexto macroeconómico europeo vuelve a deteriorarse, lo que viene a sumarse a la debilidad del crecimiento derivada de la pandemia y de la crisis energética que se produjo tras la invasión de Ucrania por parte de Rusia. Cuatro años después, vemos que la producción industrial en Alemania, que es la mayor economía de Europa, continúa debilitándose, lo que pone de manifiesto los problemas estructurales a los que se enfrenta la región.

Germany, Industrial Production, Constant Prices, SA

Fuente: Macrobond, junio de 2026

Europa vuelve a situarse en el epicentro de todas las tensiones, ya que la crisis energética derivada del conflicto en Oriente Próximo impulsa al alza la inflación y los costes de financiación están empezando a aumentar. La persistente presión sobre el coste de la vida podría consolidar comportamientos de los consumidores como retrasar el gasto u optar por alternativas más baratas. Los aranceles estadounidenses complican aún más el panorama, y la inestabilidad adicional derivada de la guerra entre Estados Unidos e Irán podría ampliar el universo de inversión en Italia y el Reino Unido, dada su dependencia del petróleo procedente del Golfo.

Estos factores podrían traducirse en problemas de oferta y demanda, o simplemente en un aumento de los costes, lo que presionaría los márgenes y afectaría a la rentabilidad. A su vez, las compañías con liquidez limitada y un nivel elevado de apalancamiento podrían necesitar refinanciación u otras soluciones de financiación, lo que ampliaría aún más el universo de inversión para los inversores en deuda en dificultades.

3. Menor competencia entre inversores, mejores condiciones: la inversión en situaciones especiales en Europa está dominada por varios fondos de gran tamaño. Cuando las compañías del mercado medio europeo han de acometer procesos de reestructuración o refinanciación, el volumen de inversión requerido suele ser inferior al de las empresas de mayor tamaño. La rentabilidad potencial de estas operaciones suele tener un impacto menor en los grandes fondos de inversión, lo que reduce su interés por participar en ellas. Por lo tanto, la competencia entre los inversores potenciales se reduce, y las condiciones y el potencial de rentabilidad suelen resultar más atractivos.

Fuerte aumento del universo de inversión

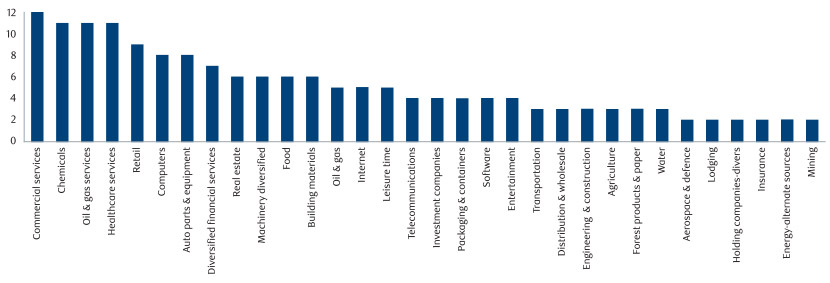

El número de oportunidades de inversión que mantenemos en nuestra lista de seguimiento se ha disparado durante el último año; hoy triplica su tamaño medio y marca su nivel más alto hasta la fecha.

Las oportunidades no se limitan a uno o dos sectores concretos, sino que abarcan una amplia variedad de industrias. En episodios de tensión anteriores, el impacto se concentró en mayor medida en determinados sectores, pero hoy casi todos ellos están experimentando algún tipo de impacto.

Un universo de inversión en expansión en una variedad más amplia de sectores

Fuente: RBC BlueBay, febrero de 2026. Los sectores mostrados se incluyen únicamente con fines ilustrativos; no representan el conjunto completo de sectores.

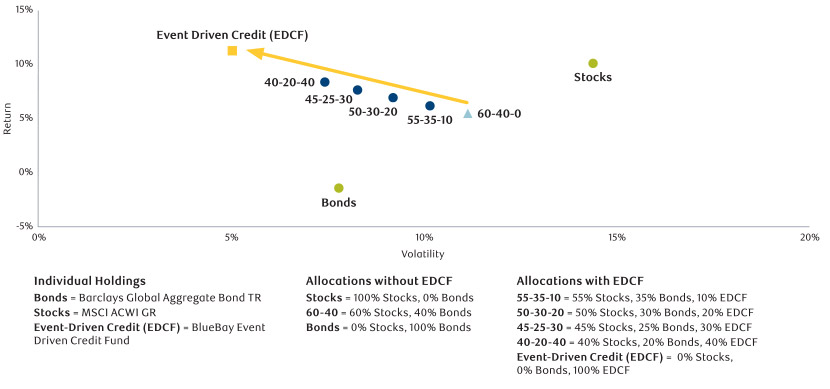

La inversión en situaciones especiales tiene cabida en casi cualquier cartera

Nuestra labor de análisis demuestra el potencial de una asignación a situaciones especiales en la construcción de carteras de inversión. La incorporación de una clase de activo que ofrece una rentabilidad absoluta atractiva y una baja correlación con las posiciones tradicionales permite a los inversores mejorar la eficiencia total de la cartera.

Hemos utilizado un enfoque de frontera eficiente en el que hemos representado en azul el perfil de riesgo/rentabilidad de conceptos sencillos de carteras tradicionales y lo hemos comparado con una asignación creciente al BlueBay Event Driven Credit Fund. Estos datos analizan el riesgo y la rentabilidad a cinco años, y muestran una mayor rentabilidad ajustada al riesgo a medida que va aumentando la exposición al crédito en situaciones especiales. Así, los datos ponen de manifiesto cómo la exposición al fondo aumentó la rentabilidad ajustada al riesgo, lo que ilustra su potencial de diversificación.

En resumen: la incorporación de esta estrategia a la cartera de inversión ha mejorado históricamente la rentabilidad, sin un aumento proporcional del riesgo.

Las rentabilidades obtenidas en el pasado no constituyen indicación alguna de rentabilidades futuras

La exposición a situaciones especiales puede mejorar la eficiencia de la cartera

Fuente: Morningstar. Información desde el 1 de abril de 2021 al 31 de marzo de 2026. Las cifras muestran una rentabilidad hipotética. Las rentabilidades hipotéticas no constituyen un indicador fiable de rentabilidades futuras. Metodología: diversas asignaciones al índice MSCI ACWI GR, al Bloomberg Global Aggregate Bond TR y al fondo BlueBay Event-Driven Credit Fund (EDCF). Reequilibrio anual de todas las carteras a cierre de año. La información es histórica y se proporciona únicamente a efectos ilustrativos. A efectos de ofrecer una comparación representativa para un inversor típico, la rentabilidad refleja la rentabilidad bruta real en EUR del fondo desde su lanzamiento hasta enero de 2023, cubierta a USD, y calculada neta de comisiones según las condiciones estándar de la clase de acción F USD: comisión de gestión del 1,25% y comisión de rentabilidad del 20%. A partir de 2023, se utiliza la rentabilidad neta real de la clase de acción F USD: comisión de gestión del 1,25% y comisión de rentabilidad del 20%. Las rentabilidades obtenidas en el pasado no constituyen indicación alguna de rentabilidades futuras; la negociación con derivados conlleva un riesgo sustancial de pérdida.

Situaciones especiales: una oportunidad de inversión permanente

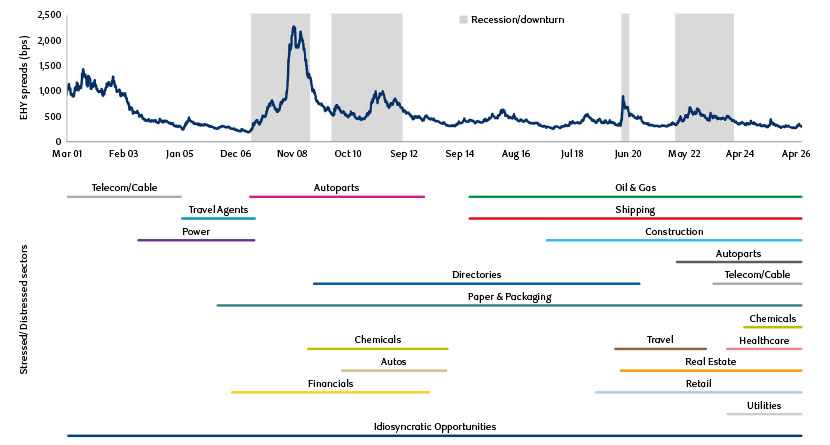

El número de oportunidades en el segmento de la deuda en dificultades tiende a repuntar en periodos de recesión, pero existe un flujo continuo de compañías y sectores que pasan por situaciones complicadas, incluso entre ciclos.

Este tipo de oportunidades se presentan de forma constante a lo largo de los distintos ciclos económicos, aunque la naturaleza concreta de dichas oportunidades va cambiando con el tiempo, según las condiciones macroeconómicas y también en función del sector y de los factores relativos a empresas concretas. El gráfico muestra los sectores con compañías en situaciones de estrés financiero y de deterioro profundo a lo largo del tiempo. Las situaciones especiales constituyen una oportunidad de inversión permanente, no puntual.

Oportunidad de inversión permanente

Source: ICE BofA European Currency HY Index, as at April 2026.

For illustrative purposes only. There is no assurance that any of the trends depicted or decribed herein will continue.

Oportunidad en un contexto de incertidumbre

El mercado medio europeo ofrece desde hace tiempo una oportunidad atractiva desde el punto de vista estructural para los inversores en situaciones especiales. Lo que ha cambiado ha sido la intensidad de las oportunidades potenciales. El deterioro del contexto macroeconómico, el aumento de la presión de refinanciación, la reducción de la liquidez y las tensiones sectoriales generalizadas han llevado a máximos históricos nuestra lista de oportunidades en seguimiento. El universo de inversión rara vez ha sido tan amplio ni tan visible.

Las condiciones actuales intensifican una oportunidad que no desaparece cuando las tensiones macroeconómicas remiten. Las situaciones especiales constituyen una estrategia permanente: cuando un ciclo acaba, comienza otro, y ello hace que vaya cambiando de manera constante el peso relativo de las subestrategias que invierten en situaciones de estrés financiero (stressed), de deterioro profundo (distressed) o de situaciones de tensión derivadas de circunstancias concretas (event-driven). Aquellos inversores que cuentan con los recursos y el rigor necesarios para identificar oportunidades de inversión, así como con la paciencia suficiente para esperar a que lleguen a materializarse, se han visto históricamente recompensados.

A todo ello se le suma el atractivo de la clase de activo desde la perspectiva de cartera, dada su trayectoria de atractiva rentabilidad absoluta, su baja correlación con las posiciones tradicionales y su potencial para mejorar la rentabilidad ajustada al riesgo. El atractivo de la inversión en situaciones especiales nunca ha sido tan evidente para aquellos inversores que persigan una rentabilidad sólida y menos correlacionada. Además, a diferencia de otras muchas estrategias que dependen de un entorno macroeconómico concreto para generar rentabilidad, esta está concebida como una estrategia de largo recorrido.