It’s remarkable global equity markets are up year-to-date given the extent of policy uncertainty. Jeremy Richardson explains the three potential tariff steps on the ‘Stairway to Liberation’, and discusses current market consensus and strategies to manage policy uncertainty in equity portfolios.

Key takeaways

- The ongoing debate over trade policy and tariffs continues to create uncertainty in equity markets. The strength of the market rotation from the U.S. to Europe has diminished.

- Q1 earnings were better than feared. But the range of policy outcomes remains wide and not everyone has been convinced by the recovery in equity markets.

- Recent volatility is a reminder of the risks of macro-biases in portfolios. Careful monitoring and management of these will allow portfolio returns to be driven by individual holdings, in particular, quality companies run by strong management teams.

Tariff uncertainty collided with post-election optimism earlier this year. De-regulatory supply-side policies have a deflationary bias considered positive for corporate profits. Tariffs, on the other hand, have to be paid for, pushing up prices and disrupting supply chains. Fears of recession increased, creating ‘push’ factors for capital to leave the U.S.. This is in contrast to Europe where security fears encouraged governments to prioritise rearmament spending at the same time as interest rates continued to be cut.

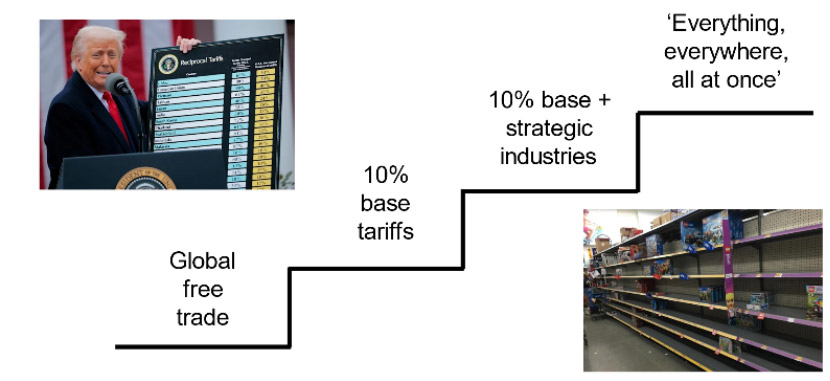

Investors and companies still don’t have the tariff policy certainty they crave. Different voices argue for different outcomes, creating a ‘stairway to liberation’ of compounding policy actions.

The tariff ‘stairway to liberation’

The first step, a 10% tariff on all imports, would be frustrating for companies, investors and consumers. But it would likely not force companies to rapidly change supply chains and would raise significant revenue for government coffers.

Some argue it doesn’t go far enough. The next step builds on the first by adding in tariffs on strategic industries, like rare earths, semiconductors and pharmaceuticals to encourage domestic re-shoring and support U.S. economic security. This is a more interventionist approach but if limited to specific business models, it is one that the market should be able to price effectively.

The final step is essentially the full ‘Rose Garden’ treatment with reciprocal tariffs based upon existing trade deficits, in particular with China, with the goal of reindustrialisation. This last step was quickly priced into equity markets after the ‘Rose Garden’ announcement elevated the risk of recession.

Empty shelves in Walmart?

The 90-day moratorium on new tariffs came as a significant relief to equity markets. The implicit signal was that the risk of ‘everything, everywhere, all at once’ is significantly reduced. It was a well-timed intervention. Orders for Halloween and Christmas retail inventory need to be placed around now if product is to arrive in time, with delays risking empty shelves at Walmart. President Trump doesn’t want to be the President who cancelled Christmas.

Market consensus has moved back down the stairway and now appears to be somewhere between steps 1 and 2.

This is a better outcome than feared in early April that has helped equity markets recover their early Spring losses. The implied risk of recession has fallen from above 50% to somewhere in the 30s% (compared to a notional probability of 20-25% in any given year).

The only certainty is uncertainty

There are a few things we don’t yet know. Firstly, will there be a long-lasting trade agreement between the U.S. and China? Scott Bessent, Treasury Secretary, has said that neither country wants to ‘decouple’ from the other, which if true may indicate a settlement is possible. But this is in conflict with the re-industrialisation objective that requires a degree of inevitable decoupling, so who is right?

Secondly, even if outline deals are agreed in the next 60 days, will they be strong enough to give companies the confidence to invest? Or will delays cause an activity air-pocket and push the U.S. into recession anyway?

Finally, might we be looking at stagflation (lower growth and inflation above 2% for longer) or a ‘Goldilocks’ economy (3% growth and inflation 2-3%) in future? The market is looking for clues, hence the focus on ‘soft’ (current survey data) and ‘hard’ (backward-looking official data) economic indicators. Results so far are somewhat ambiguous.

So far, companies’ reported Q1 earnings have been better than feared. But Q1 was arguably always a ‘pass’ given that tariffs weren’t fully announced until the beginning of Q2. Earnings estimates have held up surprisingly well, despite ongoing policy uncertainty, but profit estimates often fade through the second half. Given valuations have recovered, this is leading many investors to ask ‘now what?’

Is the ‘great rotation’ taking a summer break?

The market rotation from the U.S. to Europe feels as though it has stalled. Tech stocks and ‘retail favourites’, such as Tesla, have been doing better lately. It is probably dangerous to be too dismissive of the U.S.. The natural advantages the country has in terms of its innovation-friendly eco-system, expanding demographics and high labour productivity all still mean that anyone looking to allocate their marginal dollar will have to consider the U.S. economy. The popularity of passive investment solutions in the U.S. also continues to act as a magnet for global capital as firms look to list in a market where passive means there is a surfeit of wealthy, value-agnostic investors.

In contrast, Europe has potential, but we have yet to see sustained commitment to the type of economic reforms and liberalisation that were set out in Mario Draghi’s 2024 report. A re-ordering of spending priorities in favour of defence is making new funds available which, together with falling interest rates, is supporting hopes of an improved environment to corporate profitability. However, this is a simple transient multiplier effect to growth – sustained economic growth probably requires supply-side reforms, the appetite for which remains unclear. A useful test-case for investors to monitor is cross-border banking consolidation, such as UniCredit’s approach to Commerzbank.

We let our companies do the talking

Our approach is a focus on company fundamentals, especially quality companies run by strong management teams, as they will be more resilient and will likely be able to take advantage of industry change better than weaker competitors. It is also important not to forget risk. Recent market volatility has highlighted the dangers of taking a strong market (beta) or country (U.S. versus Europe) view. Better to diversify such macro risks, monitor positive momentum exposure by not letting position sizes drift too far and let the company holdings do the talking.

Source: Bloomberg or publicly available data, as at May 2025.