Muchos inversores siguen relacionando la deuda bancaria con la crisis financiera mundial de 2008. Sin embargo, el sector bancario europeo está hoy mucho mejor capitalizado, está sujeto a una regulación más estricta y es más rentable. Marc Stacey, gestor senior de deuda de grado de inversión, piensa que ha llegado el momento de volver a plantearse la inversión en los bonos de capital adicional de nivel 1 (AT1).

Puntos clave

- Los bancos europeos presentan hoy mayor solidez estructural que en 2008: gracias a sus mayores reservas de capital, a una supervisión normativa más estricta y a una gestión de sus balances mucho más disciplinada, los bancos europeos se enfrentan a los periodos de incertidumbre desde una posición de partida mucho más sólida.

- Una rentabilidad más previsible refuerza la capacidad de resistencia de los bancos: unos tipos de interés más altos y unas curvas de tipos más pronunciadas contribuyen al aumento de los ingresos netos por intereses, lo que permite a los bancos registrar unas cifras de beneficios más sólidas y predecibles.

- Es probable que las valoraciones de los bancos no reflejen aún plenamente la mejora que han experimentado: pese a la mayor solidez de sus fundamentales, las valoraciones de los bancos siguen estando por debajo de sus medias a largo plazo, lo que apunta a que el mercado podría no haber reconocido aún plenamente el aumento de capital y rentabilidad que han registrado las entidades.

La deuda de los bancos europeos merece un nuevo análisis

Para muchos inversores, la deuda bancaria sigue evocando recuerdos de 2008, cuando los bancos fueron el epicentro de la crisis financiera mundial. En aquel momento, los balances estaban al límite, los ratios de capital estaban muy ajustados y la confianza en el sistema financiero se había visto muy deteriorada.

Hoy, esos recuerdos chocan con una nueva oleada de incertidumbre de los inversores. En un contexto marcado por el riesgo geopolítico, las presiones inflacionistas derivadas del aumento de los precios del petróleo, las expectativas de subidas de tipos de interés y la moderación de las perspectivas de crecimiento, los inversores están revaluando la propensión al riesgo.

Por lo tanto, resulta comprensible que los inversores mantengan la prudencia en lo que se refiere a la financiación de los bancos, especialmente a través de instrumentos subordinados como los bonos de capital adicional de nivel 1 (AT1). Los AT1 son bonos perpetuos diseñados para absorber pérdidas en periodos de fuerte tensión bancaria, por lo que los inversores no deben olvidar cuáles son los riesgos que conllevan. Pero la prudencia no debería impedirnos reconocer que el sector bancario europeo actual es mucho más sólido de lo que era antes de la crisis financiera mundial.

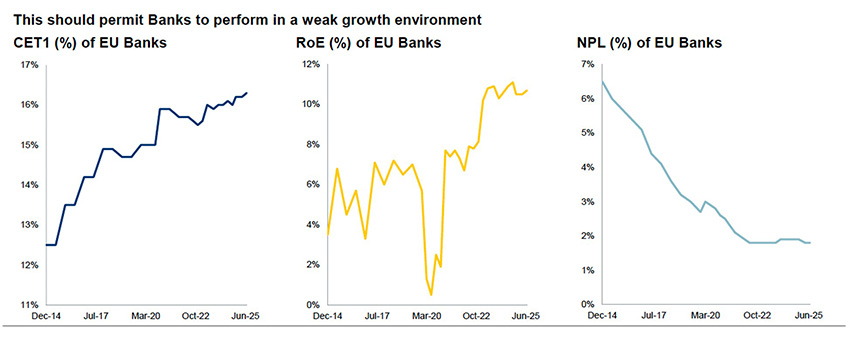

Es posible que los niveles de capital de los bancos europeos se encuentren entre los más sólidos de su historia

El punto de partida para los bancos es la adecuación del capital. El capital ordinario de nivel 1 (CET1) constituye la primera línea de absorción de pérdidas en el balance de un banco antes de que se vean afectados los titulares de deuda subordinada.

Antes de 2008, las reservas de capital de muchos bancos europeos eran mucho más reducidas. Sin embargo, desde la crisis financiera mundial, los bancos europeos se han visto sujetos a una profunda reforma normativa centrada en las exigencias de capital, la mejora de la liquidez y una supervisión más estricta, impulsada principalmente por la aplicación de Basilea III. Uno de los cambios más importantes fue la introducción de los bonos AT1 como una capa adicional de absorción de pérdidas dentro de las estructuras de capital de los bancos.

En la actualidad, los niveles de capital CET1 en el sector bancario europeo han aumentado al 16,3%1, por lo que es posible que estos niveles de capital estén entre los más sólidos de su historia. Poniéndolo en perspectiva, y utilizando un indicador anterior a la implantación de Basilea III, la capitalización de los bancos europeos se ha más que duplicado desde la crisis financiera mundial en términos de activos ponderados por riesgo2. Este aumento es importante, ya que, cuanto mayores sean las reservas de capital, mayor será la protección de los inversores en bonos AT1 dentro de la estructura de capital de los bancos.

El aumento de la rentabilidad de los bancos ofrece una capa adicional de protección a los inversores

Durante varios años tras la crisis de 2008, los bancos europeos se asociaron con una baja rentabilidad para los accionistas, una normativa estricta y una capacidad limitada de generación de beneficios. La situación ha cambiado. En la actualidad, unos tipos de interés más altos y unas curvas de tipos más pronunciadas contribuyen al aumento de los ingresos netos por intereses, mientras que el incremento de los beneficios ofrece a los bancos una mayor capacidad para absorber pérdidas crediticias, reponer capital y conceder financiación.

Para los inversores de renta fija, unas perspectivas de beneficios más favorables y una tasa de morosidad más contenida favorecen que el sector esté en mejores condiciones para hacer frente a una ralentización del crecimiento. En conjunto, todo ello apunta a un contexto mucho más favorable para el sector bancario (véase el gráfico 1).

Fundamentales: tan sólidos como siempre

Fuente: Autoridad Bancaria Europea, a enero de 2026.

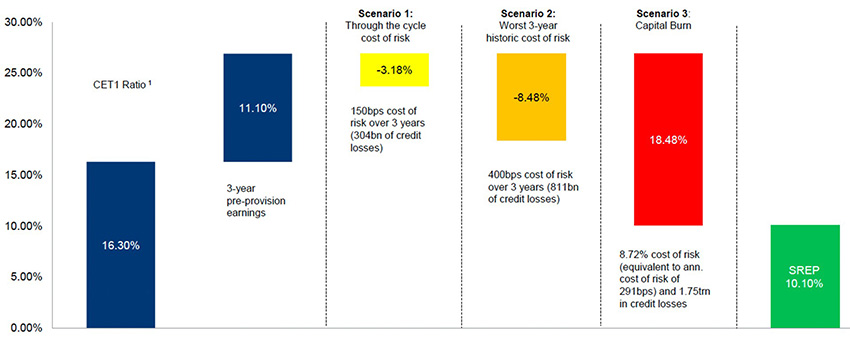

No solo han mejorado los beneficios, sino también los modelos de negocio

La composición de los beneficios bancarios también ha mejorado. Los bancos europeos ya no son las mismas entidades que en 2008: ahora dependen en menor medida de la negociación por cuenta propia y de otras fuentes de ingresos más volátiles. Hoy presentan una estructura de beneficios más predecible y con rasgos propios de un servicio público, con un enfoque más claro en el crédito, el asesoramiento y la disciplina del balance. El gráfico 2 muestra cómo esta base más sólida de capital y rentabilidad puede ofrecer cierta protección a los inversores en deuda subordinada en distintos escenarios de tensión de los mercados.

Gráfico 2: Escenarios de tensión de las reservas de capital

Fuente: RBC GAM, BCE, a 31 de diciembre de 2025.

Fuente: RBC GAM, BCE, a 31 de diciembre de 2025.

SREP: Proceso de Revisión y Evaluación Supervisora.

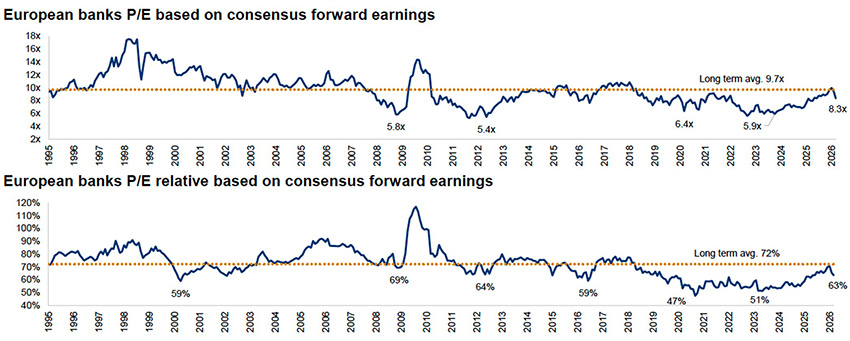

Es posible que las valoraciones no reflejen la situación actual de los bancos europeos

Pese al aumento del capital y de la rentabilidad, las valoraciones de los bancos europeos siguen estando por debajo de sus medias a largo plazo (véase el gráfico 3). En nuestra opinión, ello apunta a que el mercado podría no haber reconocido aún plenamente la mejora de los fundamentales. Para los inversores en bonos AT1, esto significa que el aumento del capital y de la rentabilidad respalda la estructura de capital de los bancos, aun cuando las valoraciones no reflejen aún plenamente dicho cambio.

Gráfico 3: Los PER absolutos y relativos apuntan a valoraciones reducidas de los bancos

Fuente: Autonomous Research, Bloomberg, Datastream, a 20 de marzo de 2026.

Datos basados en los beneficios de consenso; los datos históricos se basan en el segundo ejercicio fiscal. Los datos desde 2010 se basan en la información de Bloomberg y corresponden a una estimación combinada de beneficios a dos años vista.

Inversión en bonos AT1

Para los inversores en bonos AT1, las rentabilidades cercanas al 10% que ofrecen actualmente estos instrumentos podrían seguir reflejando una valoración basada en la imagen de los bancos en 2008, y no en su situación actual. Al quedar excluidos de los principales índices de renta fija, los bonos AT1 siguen presentando unas valoraciones atractivas frente a segmentos adyacentes de la estructura de capital de los bancos, lo que podría ofrecer un diferencial adicional de rentabilidad.

Eso no quiere decir que estén exentos de riesgos. Sus cupones podrían cancelarse, cabe la posibilidad de que no se amorticen anticipadamente en la fecha esperada y, en situaciones extremas, pueden absorber pérdidas, por lo que la selección de títulos, el análisis de los emisores y la interlocución con las entidades de regulación resultan esenciales.

Los bonos AT1 no existen de forma aislada. Su atractivo depende de la solidez de los bancos que los respaldan. Los bancos europeos ya no son las instituciones frágiles y escasamente capitalizadas que los inversores recuerdan de 2008. Los riesgos de los AT1 siguen exigiendo un análisis exhaustivo, pero la solidez del capital, la rentabilidad y la calidad del modelo de negocio del sector han mejorado. Dicho cambio merece un nuevo análisis por parte de los inversores.

1 Autoridad Bancaria Europea. Informe con fecha de 23 de marzo de 2026.

2 Banco Central Europeo. Informe con fecha de 11 de junio de 2025.