Per molti investitori, il debito bancario richiama ancora alla mente la crisi finanziaria globale del 2008. Tuttavia, oggi il settore bancario europeo è meglio capitalizzato, più rigidamente regolamentato e più redditizio. Per questo motivo, Marc Stacey, Senior IG Portfolio Manager, ritiene che sia arrivato il momento di riconsiderare gli AT1.

Punti chiave

- Le banche europee sono strutturalmente più solide rispetto al 2008: grazie a maggiori riserve di capitale, a una supervisione regolamentare più rigorosa e a una disciplina di bilancio notevolmente migliorata, oggi possono affrontare fasi di incertezza partendo da una posizione molto più forte.

- Una redditività più prevedibile rappresenta un importante elemento di resilienza: tassi di interesse più elevati e curve dei rendimenti più ripide sostengono il margine di interesse netto, contribuendo a generare utili più solidi e prevedibili.

- Le valutazioni delle banche potrebbero non riflettere ancora pienamente i miglioramenti compiuti: nonostante fondamentali più solidi, le valutazioni azionarie del settore restano inferiori alle medie di lungo periodo, suggerendo che il mercato non abbia ancora riconosciuto appieno il supporto derivante da una maggiore capitalizzazione e redditività.

Il debito è un tema sensibile, ma le banche europee meritano di essere guardate con occhi nuovi

Per molti investitori, il debito bancario riporta ancora alla mente il 2008, quando le banche erano al centro della crisi finanziaria globale (GFC). All’epoca, i bilanci erano sotto pressione, i coefficienti patrimoniali limitati e la fiducia nel sistema finanziario fortemente compromessa.

Oggi quei ricordi si scontrano con una nuova fase di incertezza per gli investitori. Con il rischio geopolitico tornato al centro dell’attenzione, le pressioni inflazionistiche legate ai prezzi del petrolio, le aspettative di ulteriori rialzi dei tassi e un rallentamento della crescita stanno spingendo gli investitori a rivalutare la propria propensione al rischio.

È quindi comprensibile che gli investitori restino cauti nel finanziare le banche, soprattutto attraverso strumenti subordinati come le obbligazioni Additional Tier 1 (AT1). Gli AT1 sono obbligazioni perpetue progettate per assorbire perdite in caso di forte stress bancario, e i relativi rischi non devono essere sottovalutati. Tuttavia, cautela non significa continuare a guardare al settore bancario europeo odierno con la lente pre-crisi finanziaria.

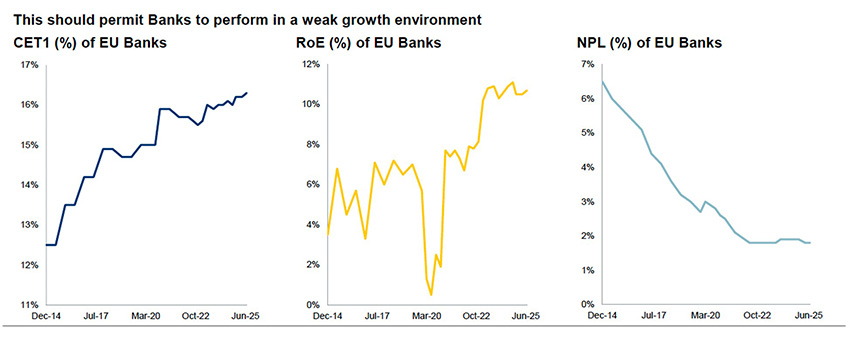

I livelli di capitale delle banche europee sono probabilmente tra i più solidi di sempre

Per le banche, il punto di partenza è l’adeguatezza patrimoniale. Il capitale Common Equity Tier 1 (CET1) rappresenta il primo cuscinetto di assorbimento delle perdite nel bilancio di una banca, prima che vengano coinvolti gli obbligazionisti subordinati.

Prima del 2008, molte banche europee operavano con riserve patrimoniali molto più limitate. Dopo la crisi finanziaria globale, tuttavia, il settore bancario europeo è stato interessato da una profonda revisione normativa focalizzata su requisiti patrimoniali più severi, maggiore liquidità e una supervisione più rigorosa, principalmente attraverso l’implementazione di Basilea III. Tra i cambiamenti più rilevanti vi è stata proprio l’introduzione delle obbligazioni AT1 come ulteriore livello di assorbimento delle perdite nella struttura del capitale bancario.

Oggi i livelli di CET1 del settore bancario europeo hanno raggiunto il 16,3%1, portando la capitalizzazione del sistema, probabilmente, ai livelli più solidi di sempre. Per dare un termine di paragone, utilizzando una misura più ampia precedente a Basilea III, dalla crisi finanziaria globale la capitalizzazione delle banche europee è più che raddoppiata in rapporto agli attivi ponderati per il rischio2. Questo è importante perché maggiore è il cuscinetto di capitale, maggiore è la protezione per gli investitori AT1 nella struttura del capitale bancario.

La crescita della redditività bancaria rappresenta un ulteriore livello di protezione per gli investitori

Per diversi anni dopo la crisi del 2008, le banche europee sono state associate a rendimenti deboli per gli azionisti, regolamentazione onerosa e limitata capacità di generare utili. Oggi questo scenario è cambiato. Tassi di interesse più elevati e curve dei rendimenti più inclinate sostengono il margine di interesse netto, mentre utili più robusti offrono alle banche una maggiore capacità di assorbire perdite sui crediti, ricostruire capitale e continuare a erogare finanziamenti.

Per gli investitori obbligazionari, questa prospettiva positiva sugli utili, insieme a livelli contenuti di crediti deteriorati, rende il settore meglio posizionato per affrontare una crescita economica più debole. Nel complesso, questo delinea un contesto molto più sano per il settore bancario.

Fondamentali: solidi come non mai

Fonte: EBA, a gennaio 2026.

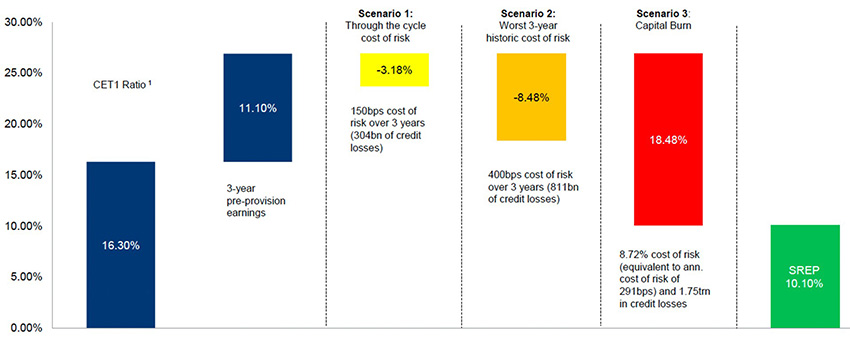

Non solo gli utili, ma anche i modelli di business sono migliorati

Anche la composizione degli utili bancari è cambiata in meglio. Le banche europee non sono più le stesse del 2008: dipendono meno dal proprietary trading e da altre fonti di ricavi più volatili. Oggi presentano una struttura degli utili più prevedibile e simile a quella di una utility, con una maggiore focalizzazione su attività di lending, consulenza e disciplina di bilancio. Il grafico 2 mostra come questa base più solida in termini di capitale e redditività possa offrire una certa protezione agli investitori in debito subordinato in diversi scenari di stress.

Grafico 2: Stress test sui buffer patrimoniali

Fonte: RBC GAM, ECB, al 31 dicembre 2025.

Fonte: RBC GAM, ECB, al 31 dicembre 2025.

SREP = Supervisory Review and Evaluation Process (Processo di revisione e valutazione prudenziale).

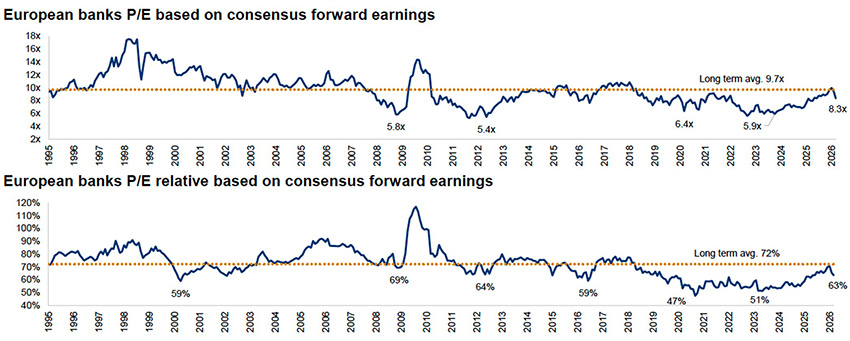

Le valutazioni non sembrano ancora riflettere pienamente la situazione attuale delle banche europee

Nonostante una maggiore capitalizzazione e migliori rendimenti, le valutazioni azionarie delle banche europee restano inferiori alle medie di lungo periodo (grafico 3). A nostro avviso, questo suggerisce che il mercato non abbia ancora pienamente riconosciuto il miglioramento dei fondamentali del settore bancario. Per gli investitori in AT1, ciò significa che capitale più solido e maggiore redditività continuano a sostenere la struttura patrimoniale delle banche, anche se le valutazioni non riflettono ancora completamente questo cambiamento.

Grafico 3: I rapporti P/E assoluti e relativi indicano che le banche sono convenienti

Fonte: Autonomous Research, Bloomberg, Datastream, al 20 marzo 2026.

Sulla base degli utili consensus; i dati storici si basano sul secondo esercizio fiscale. Dal 2010 i dati Bloomberg fanno riferimento agli utili forward blended a due anni.

La tesi a favore degli AT1

Per gli investitori in AT1, i rendimenti a una cifra medio-alta disponibili al momento della stesura di questo contenuto potrebbero riflettere ancora una valutazione “legacy” delle banche, legata a come erano nel 2008 e non a come sono oggi. Inoltre, essendo esclusi dai principali indici obbligazionari, gli AT1 appaiono ancora interessanti in termini relativi rispetto ad altre componenti della struttura del capitale bancario, offrendo potenziale rendimento aggiuntivo.

Questo non significa che siano strumenti privi di rischio. Le cedole AT1 possono essere cancellate, le obbligazioni potrebbero non essere richiamate quando previsto e, in eventi estremi, possono assorbire perdite. Per questo motivo, selezione attiva del credito, analisi degli emittenti e attenzione agli aspetti regolamentari restano fondamentali.

Gli AT1 non operano in un vuoto. La loro validità come investimento dipende dalla solidità delle banche sottostanti. Le banche europee non sono più le istituzioni fragili e sottocapitalizzate che molti investitori ricordano dal 2008. I rischi degli AT1 devono ancora essere attentamente valutati, ma la solidità patrimoniale, la redditività e la qualità del modello di business del settore sono nettamente migliorate. Ed è un cambiamento che merita di essere guardato con occhi nuovi.

1 European Banking Authority. Report del 23 marzo 2026.

2 Banca Centrale Europea. Report dell’11 giugno 2025.