Location

Please select your investor type by clicking on a box:

Terms & conditions

We are unable to market if your country is not listed.

You may only access the public pages of our website.

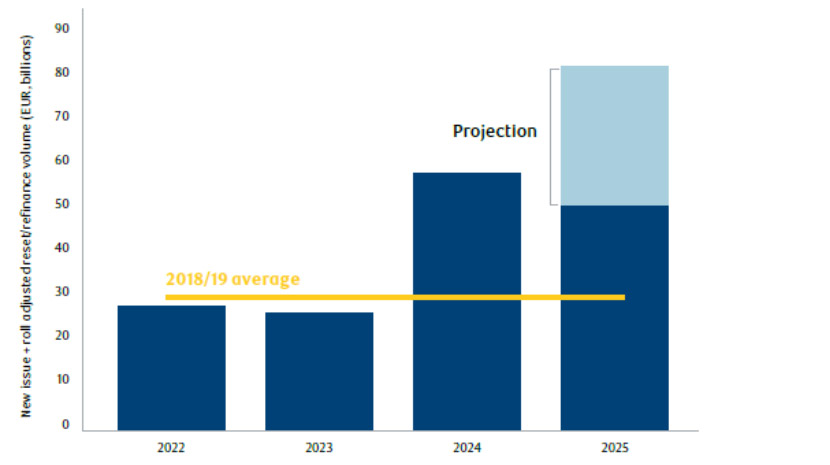

European CLO issuance remained robust in 2022 and 2023, despite volatile market conditions. Many of the deals priced during this period are now exiting their non-call periods and are being refinanced through resets. However, not all investors in the original 2022/2023 deals are participating in these resets. This has resulted in excess reset volume, adding to the already elevated levels of new issuance seen this year. Consequently, the market has experienced an oversupply of CLOs.

Source: RBC GAM, 9fin, as at 2 September 2025. European CLO supply based on new issue volume plus refinance/reset volumes adjusted for rolls. For illustrative purposes only. There is no assurance that any of the trends depicted or described herein will continue.

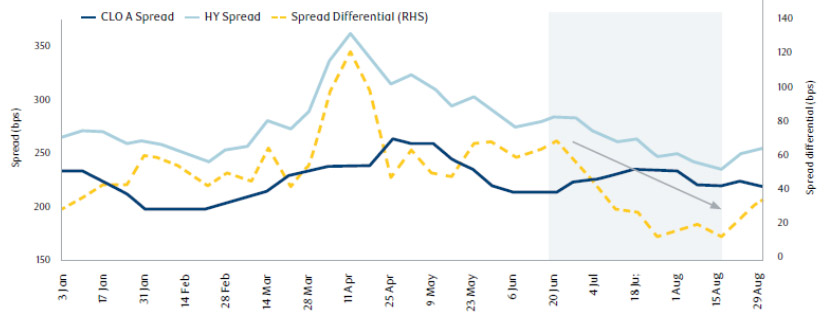

The combination of high reset volume and strong new issuance over the summer months drove spread widening in primary markets, particularly in the single-A tranche. In mid-June, CLO single-A spreads began to widen gradually, reaching 240-250 bps by August, compared to 200 bps at the start of the year. Interestingly, while CLO single-A spreads were widening, broader credit markets were tightening, as reflected in the BB-European High Yield Index, which tightened to around 260 bps. This led to a significant compression in the spread basis between single-A CLOs and BB-European High Yield bonds, narrowing to just 10-20 bps.

Source: RBC GAM, Bloomberg, Wells Fargo, as at 29 August 2025. For illustrative purposes only. There is no assurance that any of the trends depicted or described herein will continue.

We identified this market dislocation early and were well-positioned to act, with cash available across our strategies. In the first half of the year, we maintained very selective exposure to the primary market, favouring shorter-duration and deleveraging profiles amid growing macroeconomic uncertainty. As the macro environment stabilised and this unique opportunity emerged, we actively added significant volumes of high-quality European CLOs in the primary market, leveraging this dislocation to generate alpha.

Please choose from the following

We are unable to market if your country is not listed.

You may only access the public pages of our website.