In special situations investing, volatility and financing stress aren't just challenges to navigate, they're the conditions that make compelling returns possible.

Key takeaways:

- A structurally fertile hunting ground: Europe’s mid-market continues to offer a plethora of opportunities, given reduced financing options for these companies and reduced competition among investors.

- A record-high opportunity set: our special situations team’s watchlist of opportunities was already at a record high, even before the Iran conflict.

- A compelling portfolio diversifier: our analysis shows that adding a special situations allocation has the potential to improve risk-adjusted returns across various portfolio constructions, driven by historically attractive absolute returns and low correlation to traditional asset classes.

Special situations investing involves identifying companies facing financing challenges or a particular event, and where the debt may be priced too cheaply relative to the likely outcome.

These strategies thrive on refinancing stress, forced or technical dislocations, complex situations, liquidity gaps, event-specific situations, and wider macroeconomic volatility. In a world of increasing frequency of macroeconomic ‘shocks’, the opportunity set for special situations continues to be compelling.

We explain why the middle-market opportunity in Europe is so attractive, why our watchlist is at a record high, and how a strategic allocation to special situations can benefit investor portfolios.

Why the European mid-market is so attractive

We believe the European middle-market will continue to be fertile ground for investors.

There are three main reasons for this:

1. Structurally underserved: middle-market companies in Europe can broadly be defined as those with capital structures ranging from US$100 to US$500 million of debt. They are generally less diversified by product and geography, which reduces their resilience under stress. They often have less access to finance than larger peers, meaning those already paying elevated rates on existing debt access can struggle to refinance through the capital markets. Consequently, they are more reliant on banks, which have tightened credit standards and requirements in recent years. This creates a natural role for special situations investors.

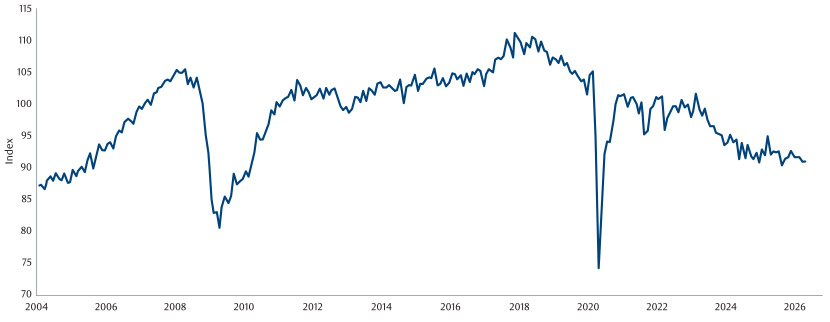

2. Cyclical pressure driving an expanding opportunity set: the macro backdrop in Europe is deteriorating again, compounding existing growth weakness stemming from Covid and the energy shock following Russia’s invasion of Ukraine. Four years on from this event, it is notable that industrial production in Europe’s largest economy, Germany, continues to deteriorate, reflecting the structural challenges the region faces.

Germany, Industrial Production, Constant Prices, SA

Source: Macrobond, June 2026

The region once again finds itself at the epicentre of distress as the Middle East energy supply crisis drives inflation higher and borrowing costs begin to rise. An ongoing cost-of-living crisis could entrench consumer behaviours such as delaying spending or trading down. US tariffs are an added headwind. The additional disruption from the US-Iran war is also likely to increase the opportunity set in Italy and the UK due to their respective dependence on oil from the Gulf.

These factors risk feeding through to demand and/or supply issues, or simply cost inflation, pressuring margins and profitability. Those companies with limited liquidity and elevated leverage may in turn require refinancing or other forms of support, creating an expanding opportunity set for distressed investors.

3. Less investor competition, better terms: special situations investing in Europe is dominated by some very large funds. When European middle-market companies require restructuring or refinancing, the required investment sizes are typically smaller than for larger peers. For the largest investment funds, the potential returns from these smaller deals are less impactful at the overall fund level, reducing their appetite to participate. As a result, competition between potential investors is lower, and the terms and return potential are typically more attractive.

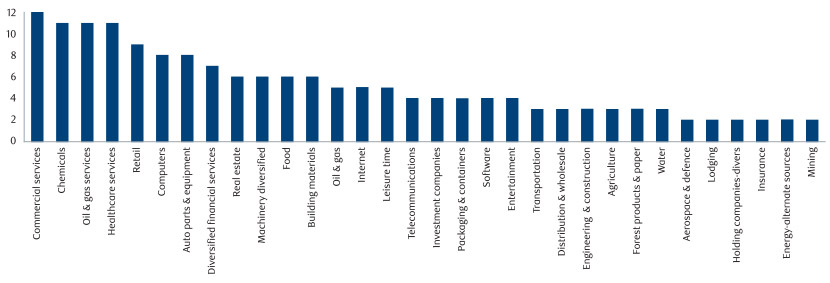

Is the number of investible opportunities set to explode?

The absolute number of investment opportunities on our watchlist has soared in the last year, and at three times the average size, is at a record high.

These are not a feature of one or two sector issues; the opportunity set is diverse, spanning a broad range of industries. Whilst previous downturns might have been more sector-specific, today almost every sector is seeing some form of impact.

A widening opportunity set across a wider array of industries

Source: RBC BlueBay, February 2026. Selected industries shown for illustrative purposes – full breadth of industries is not shown.

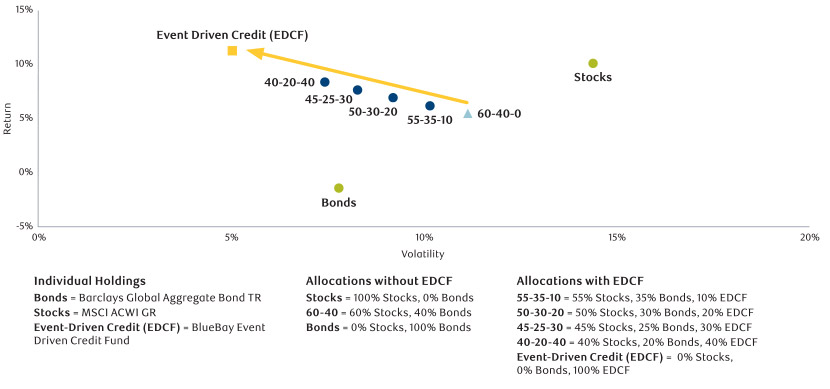

Why special situations has a role in almost any portfolio

Our analysis below demonstrates the potential of a special situations allocation in a portfolio construction. By adding an asset class with attractive absolute returns and low correlation to traditional holdings, investors can improve overall portfolio efficiency.

Taking an efficient frontier framework, we plotted the risk/return profile of simple traditional portfolio concepts in blue, and compared these with an increasing allocation to BlueBay Event Driven Credit Fund. This data looks at five-year risk and return, showing higher risk-adjusted returns as the allocation to event-driven credit increased. This shows that adding an allocation to the fund improved the risk-adjusted returns, illustrating its diversification potential.

In short, adding this strategy to a portfolio has historically improved returns without a proportionate increase in risk.

Past performance is not indicative of future results

How a special situations allocation has potential to improve portfolio efficiency

Source: Morningstar. Data from 01/04/2021 to 31/03/2026. These figures show hypothetical performance. Hypothetical performance is not a reliable indicator of future results. Methodology: Different allocations of MSCI ACWI GR, Bloomberg Global Aggregate Bond TR, and BlueBay Event-Driven Credit Fund (EDCF). All portfolios are rebalanced annually at year end. All information is historical and for illustrative purposes only. To provide representative comparison for a typical investor, the performance represents the actual EUR gross performance of the Fund since inception to January 2023, hedged into USD, and calculated net of fees assuming the standard terms of the USD F Share Class (1.25% management fee and 20% performance fee). From 2023 onwards the actual net performance of the USD F Shareclass (1.25% management fee and 20% performance fee) is used. Past performance is not indicative of future performance, derivatives trading involves a substantial risk of loss.

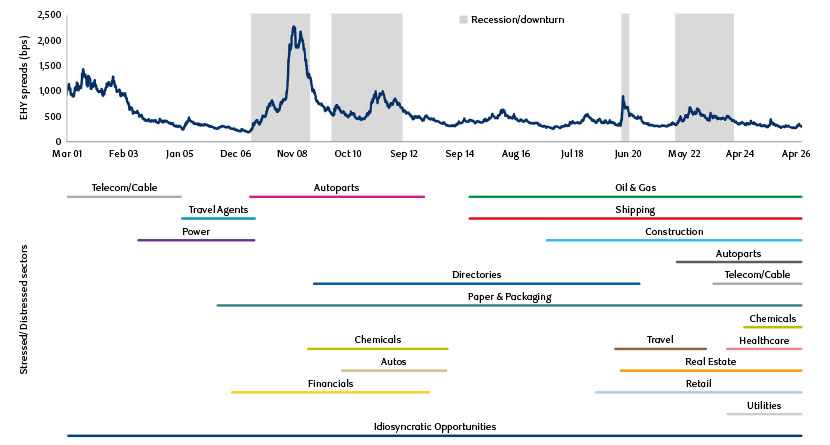

Special situations: an evergreen investment opportunity

The number of distressed opportunities tends to spike in recessions, but there is a continuous stream of troubled sectors and companies, even between cycles.

These types of opportunities constantly present themselves through different economic cycles, though the specific nature of those opportunities shifts over time, shaped by macroeconomic conditions and by sector, industry and company-specific factors. The chart below highlights the sectors with stressed or distressed companies over time. Special situations are an evergreen investment opportunity as opposed to a momentary one.

The evergreen investment opportunity

Source: ICE BofA European Currency HY Index, as at April 2026.

For illustrative purposes only. There is no assurance that any of the trends depicted or decribed herein will continue.

Opportunity out of uncertainty

Europe's mid-market has long offered a structurally compelling case for special situations investors. What has changed is the intensity of potential opportunities. A deteriorating macroeconomic backdrop, rising refinancing pressure, dwindling liquidity and broad-based sectoral stress have driven our watchlist to a record high. The opportunity set has rarely been this visible, or this broad.

Today's conditions amplify an opportunity that doesn't disappear when macro stress eases. Special situations is an evergreen strategy: as one cycle fades, another begins, and the balance shifts continuously between stressed, distressed, and event-driven sub-strategies. For investors with the resources and rigour to identify opportunities, and the patience to see them through, the rewards have historically been consistent.

Added to this is the portfolio case, given a track record of attractive absolute historical returns, low correlation to traditional asset holdings, and the potential to improve risk-adjusted outcomes. For investors seeking resilient, less correlated returns, the case for special situations has rarely been clearer. And unlike many strategies that depend on a specific macroeconomic environment to deliver, this one is built to last.

Certain information contained herein (the “Information”) is sourced from/copyright of MSCI Inc., MSCI Solutions LLC, or their affiliates (“MSCI”), or information providers (together the “MSCI Parties”) and may have been used to calculate scores, signals, or other indicators. The Information is for internal use only and may not be reproduced or disseminated in whole or part without prior written permission. The Information may not be used for, nor does it constitute, an offer to buy or sell, or a promotion or recommendation of, any security, financial instrument or product, trading strategy, or index, nor should it be taken as an indication or guarantee of any future performance. Some funds may be based on or linked to MSCI indexes, and MSCI may be compensated based on the fund’s assets under management or other measures. MSCI has established an information barrier between index research and certain Information. None of the Information in and of itself can be used to determine which securities to buy or sell or when to buy or sell them. For regulatory disclosures mandated under the EU ESG Rating Activities Regulation (Regulation (EU) 2024/3005), please visit www.msci.com/legal/sustainability-and-climate-resources-and-disclosures for methodology and organizational disclosures and https://one.msci.com for rating level disclosures. The Information is provided “as is” and the user assumes the entire risk of any use it may make or permit to be made of the Information. No MSCI Party warrants or guarantees the originality, accuracy and/or completeness of the Information and each expressly disclaims all express or implied warranties. No MSCI Party shall have any liability for any errors or omissions in connection with any Information herein, or any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.