Location

Please select your investor type by clicking on a box:

Terms & conditions

We are unable to market if your country is not listed.

You may only access the public pages of our website.

For many investors, bank debt still brings back memories of 2008, when banks sat at the centre of the Global Financial Crisis (GFC). At the time, balance sheets were stretched, capital ratios were tight, and confidence in the financial system was badly shaken.

Today, those memories are colliding with a fresh round of investor uncertainty. With geopolitical risk once again in focus, oil price-led inflation pressure, rising interest rate expectations, and a moderating growth outlook are all prompting investors to reassess risk appetite.

It is therefore understandable that investors remain cautious when lending to banks, particularly through subordinated instruments such as Additional Tier 1 (AT1) bonds. AT1s are perpetual bonds designed to absorb losses in periods of severe bank stress, so their risks should not be ignored. But caution should not mean looking at today’s improved European banking sector through a pre-GFC lens.

For banks, the starting point is capital adequacy. Common Equity Tier 1 (CET1) capital provides the first loss-absorbing cushion on a bank’s balance sheet before subordinated bondholders are affected.

Before 2008, many European banks operated with much thinner equity cushions. Since the GFC, however, European banks have faced a comprehensive regulatory overhaul focused on capital requirements, improved liquidity, and stronger supervision, driven mainly by Basel III implementation. Among the key changes, AT1 bonds were introduced as an additional loss-absorbing layer within bank capital structures.

Today, CET1 levels across the European banking sector have risen to 16.3%1, making capital levels arguably among the strongest they have ever been. To put that in perspective, using a broader pre-Basel III measure, since the GFC, the capitalisation of European banks has more than doubled in terms of their risk-weighted assets2. That matters, as the larger the equity buffer, the greater the protection beneath AT1 investors in the bank capital structure.

For several years after the 2008 crisis, European banks were associated with weak shareholder returns, heavy regulation, and limited earnings power. That picture has changed. Today, higher interest rates and steeper yield curves support net interest income, while stronger earnings give banks more capacity to absorb credit losses, rebuild capital, and lend.

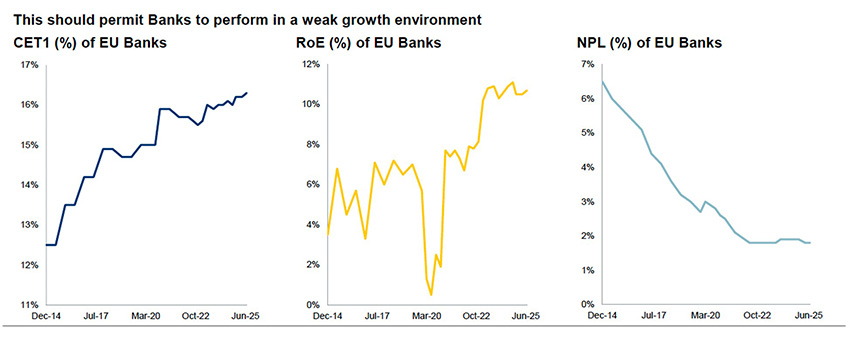

For bond investors, that constructive profit outlook, alongside contained non-performing loans, makes the sector better placed to navigate weaker growth. Taken together, this points to a much healthier banking sector backdrop (Chart 1).

Fundamentals: as robust as they have ever been

Source: EBA, as at January 2026.

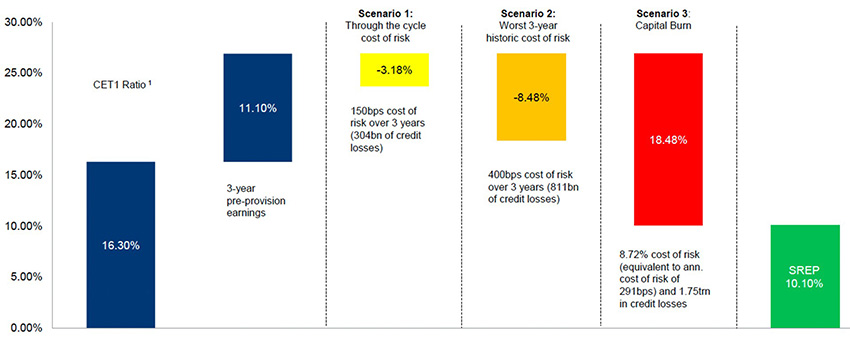

The composition of bank earnings has also changed for the better. European banks are not the same businesses they were in 2008, with less reliance on proprietary trading and other volatile revenue streams. Today, they offer a more utility-like and forecastable earnings mix, with greater focus on lending, advice, and balance sheet discipline. Chart 2 shows how this stronger capital and profitability base can offer some protection for subordinated debt investors under various stress scenarios.

Chart 2: Stressing the capital buffers

Source: RBC GAM, ECB, as at 31 December 2025.

Source: RBC GAM, ECB, as at 31 December 2025.

SREP = Supervisory Review and Evaluation Process.

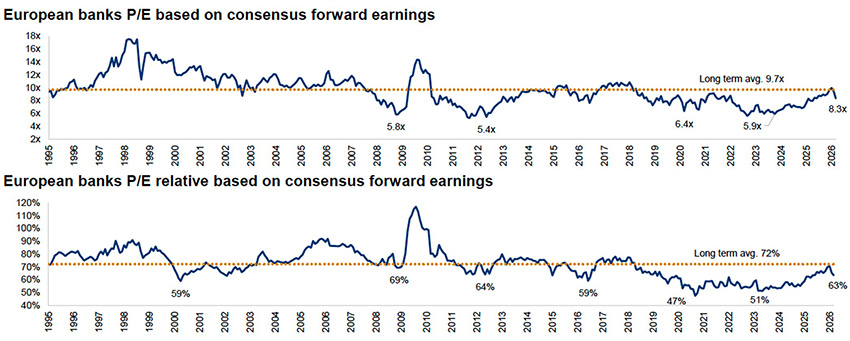

Despite stronger capital and improved returns, European bank equity valuations remain below longer-term averages (Chart 3). In our view, that suggests the market may not yet fully recognise the improvement in bank fundamentals. For AT1 investors, that means stronger capital and profitability provide support for the bank capital structure, even if valuations have yet to fully reflect that change.

Chart 3: Absolute and relative P/Es mean banks are cheap

Source: Autonomous Research, Bloomberg, Datastream, as at 20 March 2026.

Based on consensus earnings, historical data is based on the second fiscal year. Data from 2010 is based on Bloomberg and is 2-year blended forward earnings.

For AT1 investors, the high single-digit yields at the time of writing may still reflect a legacy assessment of banks as they were in 2008, and not as they are today. Excluded from mainstream fixed income indices, AT1s also arguably remain attractively valued relative to adjacent parts of the bank capital structure, creating potential for additional yield pickup.

That is not to say they are risk free. AT1 coupons can be cancelled, bonds might not be called when expected, and in extreme events, they can absorb losses. This makes active credit selection, issuer analysis, and regulatory engagement essential.

AT1s do not operate in a vacuum. Their investment case depends on the health of the banks that sit behind them. European banks are no longer the fragile, thinly-capitalised institutions that investors may remember from 2008. The risks of AT1s still need to be weighed carefully, but the sector’s capital strength, profitability, and business model quality have changed for the better. For investors, that change deserves a fresh look.

1 European Banking Authority. Report dated 23 March 2026.

2 European Central Bank. Report dated 11 June 2025.

Please choose from the following

We are unable to market if your country is not listed.

You may only access the public pages of our website.