Volatilität und Finanzierungsdruck sind charakteristisch für Special-Situation-Strategien. Doch beide stellen nicht nur Herausforderungen dar, sondern sind Voraussetzung für attraktive Renditen.

Auf einen Blick:

- Ein strukturell attraktives Anlageuniversum: Wir sehen weiterhin viel Potenzial im europäischen Mittelstand: Die Finanzierungsmöglichkeiten dieser Unternehmen sind begrenzt, der Wettbewerb unter den Investoren hat nachgelassen.

- Ein rekordgroßes Anlageuniversum: Unsere Special Situations Watchlist hatte bereits vor dem Iran-Konflikt eine Rekordlänge erreicht.

- Überzeugende Diversifizierungseigenschaften: Wie unsere Analyse zeigt, kann eine Special-Situations-Allokation die risikobereinigte Rendite verschiedener Portfoliostrukturen dank attraktiver absoluter Renditen und einer geringen Korrelation zu traditionellen Anlageklassen potenziell verbessern.

Special-Situations-Investoren suchen nach Unternehmen, die Finanzierungsschwierigkeiten haben oder mit einem bestimmten Ereignis konfrontiert sind – und deren Schulden im Verhältnis zum wahrscheinlichen Ergebnis möglicherweise zu günstig bewertet sind.

Diese Strategien schöpfen das Potenzial von Refinanzierungsengpässen, erzwungenen oder technischen Verwerfungen, komplexen Situationen, Liquiditätslücken, speziellen Ereignissen oder einer allgemein erhöhten volkswirtschaftlichen Volatilität aus. Die Zahl der makroökonomischen Schocks steigt, weshalb Special Situations an ihrer Attraktivität wohl nichts einbüßen werden.

Wir erläutern, warum der europäische Mittelstand so viel Potenzial bietet, warum unsere Watchlist noch nie so lang war und wie Investoren von einer strategischen Special-Situation-Allokation profitieren können.

Was den europäischen Mittelstand so attraktiv macht

Aus drei Gründen sind wir überzeugt, dass Investoren auch in Zukunft gute Voraussetzungen im europäischen Mittelstand finden werden.

1. Strukturelle Unterversorgung: Europäische Mittelstandsunternehmen haben in der Regel zwischen 100 und 500 Millionen US-Dollar Fremdkapital aufgenommen. Diese Unternehmen sind sowohl regional als auch nach Produkten weniger diversifiziert und daher anfälliger für Marktverwerfungen, außerdem können sie sich häufig schlechter finanzieren als größere Unternehmen. Und wer bereits hohe Zinsen für bestehende Kredite zahlt, findet womöglich keinen Zugang zum Kapitalmarkt. Daher sind mittelständische Unternehmen stärker auf Banken angewiesen – die jedoch ihre Kreditvergabeanforderungen in den letzten Jahren verschärft haben. So entsteht eine natürliche Anlagemöglichkeit für Special-Situation-Investoren.

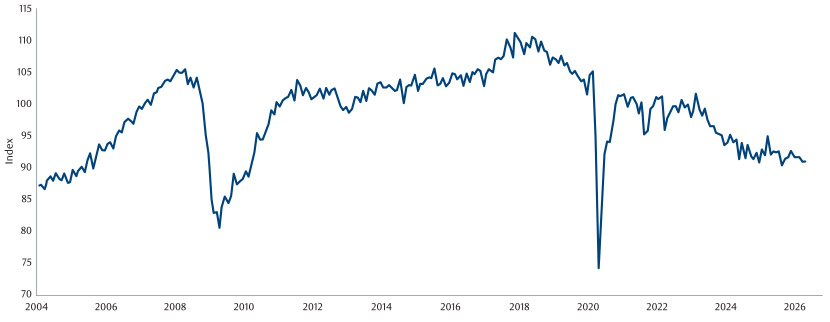

2. Die schwache Konjunktur schafft Chancen: Der erneute Konjunkturrückgang in Europa verschärft die bereits bestehende Wachstumsschwäche, die durch Covid und den Energieschock nach dem russischen Einmarsch in die Ukraine ausgelöst wurde. Vier Jahre später fällt vor allem der anhaltende Rückgang der Industrieproduktion in Deutschland, der größten europäischen Volkswirtschaft, auf, in dem sich die strukturellen Probleme des Kontinents widerspiegeln.

Germany, Industrial Production, Constant Prices, SA

Quelle: Macrobond, Juni 2026

Seit der Energiepreisschock die Inflation anheizt und die Kreditkosten steigen, herrscht in Europa einmal mehr Krisenstimmung. Steigende Lebenserhaltungskosten könnten das Verbraucherverhalten dauerhaft beeinflussen und Konsumenten veranlassen, Ausgaben aufzuschieben oder auf günstigere Produkte umzusteigen. US-Zölle erschweren die Lage, und auch der Krieg zwischen den USA und dem Iran hat die Lage verschärft. So dürften Chancen in Italien und Großbritannien entstehen, die beide in hohem Maße von Öllieferungen aus der Golfregion abhängig sind.

Diese Faktoren könnten zur Belastung sowohl für die Nachfrage- als auch für die Angebotsseite werden oder schlichtweg zu einer Kosteninflation führen und damit Margen und Rentabilität drücken. Hoch verschuldete Unternehmen mit begrenzter Liquidität sind in diesem Fall womöglich auf eine Refinanzierung oder eine andere Form von Unterstützung angewiesen und werden so zum lohnenden Ziel für Distressed-Debt-Investoren.

3. Weniger Wettbewerb unter Investoren, bessere Konditionen: Der Special- Situations-Markt in Europa wird von einigen großen Fonds dominiert. Die notwendigen Investitionssummen für eine Umstrukturierung oder Refinanzierung mittelständischer Unternehmen sind in der Regel niedriger als bei größeren Unternehmen, das Renditepotenzial dieser kleineren Transaktionen ist daher weniger attraktiv für größere Fonds, die diesem Markt entsprechend weniger Beachtung schenken. Also konkurrieren weniger Investoren um denselben Markt, was bessere Konditionen und potenziell höhere Renditen bedeutet.

Steht das Anlageuniversum vor einem Wachstumsschub?

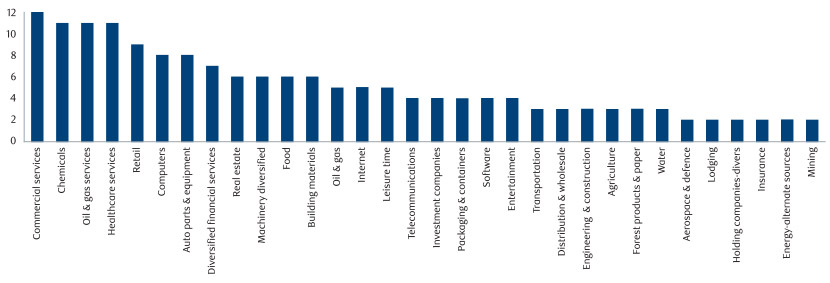

Die absolute Anzahl der Anlagemöglichkeiten auf unserer Watchlist ist im vergangenen Jahr sprunghaft angestiegen und hat mit dem Dreifachen des Durchschnittsvolumens ein Rekordhoch erreicht.

Und diese Möglichkeiten beschränken sich nicht auf ein oder zwei Sektoren. Frühere Konjunkturabschwünge mögen auf bestimmte Branchen beschränkt gewesen sein, heute dagegen sind fast alle Branchen in irgendeiner Form betroffen.

Ein wachsendes und vielfältiges Anlageuniversum

Quelle: RBC BlueBay, Februar 2026. Die aufgeführten Branchen dienen lediglich der Veranschaulichung, die gesamte Bandbreite der Branchen wird nicht dargestellt.

Warum Special Situations in fast jedes Portfolio passen

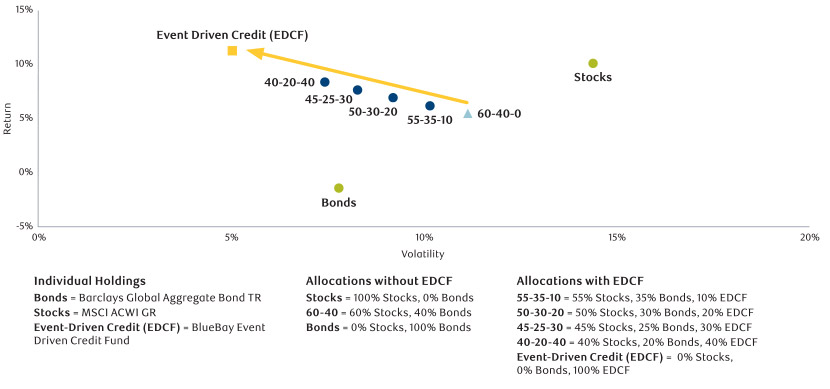

Die nachstehende Analyse verdeutlicht das Potenzial einer Special-Situation-Allokation im Portfolioaufbau. Eine Assetklasse mit attraktiven absoluten Renditen und niedriger Korrelation zu traditionellen Anlagen kann die Portfolioeffizienz erhöhen.

Mithilfe einer Effizienzgrenze haben wir das Risiko/Rendite-Profil einfacher, traditioneller Portfolios (in Blau) mit einer steigenden „BlueBay Event Driven Credit Fund“-Allokation verglichen. Diese Risiko/Renditedaten beziehen sich auf einen 5-Jahres-Zeitraum und zeigen, dass die risikobereinigten Renditen mit wachsender Event-Driven-Credit-Allokation steigen. Eine entsprechende Ergänzung hat die risikobereinigten Renditen also verbessert, was das Diversifizierungspotenzial der Assetklasse deutlich macht.

Auf den Punkt gebracht: Die Aufnahme einer Special-Situation-Strategie in ein Portfolio hätte in der Vergangenheit zu höheren Renditen ohne äquivalenten Risikoanstieg geführt.

Die Wertentwicklung in der Vergangenheit ist kein Indikator für zukünftige Ergebnisse

Höhere Portfolioeffizienz durch Special-Situation-Allokation

Quelle: Morningstar. Daten für den Zeitraum vom 01.04.2021 bis zum 31.03.2026. Diese Zahlen zeigen hypothetische Wertentwicklungen und sind kein verlässlicher Indikator für zukünftige Ergebnisse. Methodik: Unterschiedliche Gewichtungen des MSCI ACWI GR, des Bloomberg Global Aggregate Bond TR und des BlueBay Event-Driven Credit Fund (EDCF). Alle Portfolios werden jährlich zum Jahresende zurückgesetzt. Alle Angaben beziehen sich auf die Vergangenheit und dienen lediglich zu Illustrationszwecken. Um einen repräsentativen Vergleich für einen durchschnittlichen Investor zu ermöglichen, entspricht die dargestellte Wertentwicklung der tatsächlichen EUR-Brutto-Wertentwicklung des Fonds seit seiner Auflegung bis Januar 2023 (abgesichert in USD). Für die Berechnung der Wertentwicklung nach Abzug der Gebühren wurden die Standardbedingungen der Anteilsklasse I USD Perf mit einer Verwaltungsgebühr von 1,25% und einer Performancegebühr von 20% zugrunde gelegt. Ab 2023 wird die tatsächliche Nettorendite der Anteilsklasse USD F (1,25% Verwaltungsgebühr und 20% Erfolgsgebühr) zugrunde gelegt. Die Wertentwicklung in der Vergangenheit ist kein Indikator für zukünftige Ergebnisse, der Handel mit Derivaten ist mit erheblichen Verlustrisiken behaftet.

Special Situations: eine Evergreen-Anlagegelegenheit

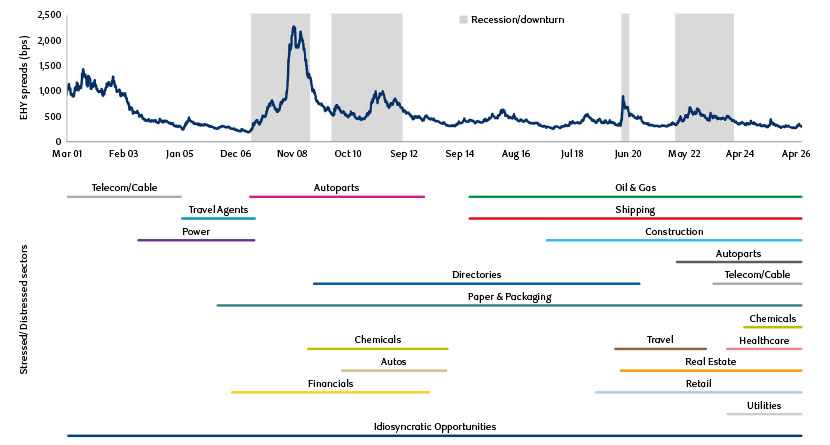

Die Zahl der notleidenden Kredite steigt in Rezessionen tendenziell sprunghaft an, doch auch zwischen den Konjunkturzyklen finden Investoren immer wieder Branchen und Sektoren, die in Schwierigkeiten geraten sind.

Derartige Chancen ergeben sich im Laufe verschiedener Konjunkturzyklen immer wieder, auch wenn sich ihre konkrete Ausprägung laufend verändert und nicht nur von dem wirtschaftlichen Umfeld, sondern auch von branchen-, sektor- und unternehmensspezifischen Faktoren abhängt. Die nachstehende Grafik bildet die Branchen ab, in denen Investoren in der Vergangenheit notleidende oder ernsthaft gefährdete Unternehmen fanden. Wie deutlich wird, sind Special Situations kein kurzfristiger Trend, sondern eine beständige Anlagemöglichkeit.

Die Evergreen-Anlagemöglichkeit

Source: ICE BofA European Currency HY Index, as at April 2026.

For illustrative purposes only. There is no assurance that any of the trends depicted or decribed herein will continue.

Wenn Unsicherheit Chancen schafft

Im europäischen Mittelstand finden Special-Situation-Investoren seit Langem strukturell überzeugende Anlagemöglichkeiten. Was sich geändert hat, ist die Anzahl dieser Möglichkeiten. Schwaches Wachstum, steigende Finanzierungskosten, schwindende Liquidität und Schieflagen in zahlreichen Sektoren sind der Grund, warum unsere Watchlist eine Rekordlänge erreicht hat. Selten zuvor waren die Chancen so offensichtlich und so vielfältig.

Das aktuelle wirtschaftliche Umfeld erweitert das Anlageuniversum auch über die konjunkturelle Schwächephase hinaus. Special Situations sind eine zeitlose Strategie: Mit dem Ende eines Zyklus beginnt ein neuer, das Gleichgewicht verschiebt sich ständig zwischen den Teilstrategien „Stressed“, „Distressed“ und „Event-Driven“. Investoren mit den notwendigen Ressourcen, die Anlagemöglichkeiten sorgfältig prüfen und Chancen identifizieren und zudem die notwendige Geduld aufbringen können, konnten mit diesen Strategien in der Vergangenheit beständige Renditen abschöpfen.

Und auch unter dem Aspekt des Portfolioaufbaus überzeugt die Assetklasse mit attraktiven absoluten Renditen, niedrigen Korrelationen zu anderen Märkten und dem Potenzial für bessere risikobereinigte Ergebnisse. Für Investoren, die beständige und möglichst unkorrelierte Renditen anstreben, waren Special-Situation-Strategien selten so attraktiv wie heute. Und im Vergleich zu vielen anderen Strategien ist ihr Erfolg weniger von den wirtschaftlichen Rahmenbedingungen abhängig.