Location

Please select your investor type by clicking on a box:

Terms & conditions

We are unable to market if your country is not listed.

You may only access the public pages of our website.

There are several key benefits that investors find attractive within emerging market debt (EMD), including diversification, yield premium and a fertile opportunity for compelling returns by sourcing alpha opportunities.

Emerging markets provide investors with access to a wider array of different economies at distinct stages of their economic cycle and, consequently, a richer variety of idiosyncratic returns drivers which can be uncorrelated to developed market economies, and often to each other. This geographical and macro-economic breadth allows for the creation of more diversified portfolios. Due to the breadth of the opportunity set, it becomes possible to find uncorrelated, idiosyncratic stories, which is particularly valuable within the context of diversifying your portfolio.

Also, the diverse economic makeup of different emerging markets can mean that some can benefit from macroeconomic trends that weigh on most developed markets. An energy price spike, for example, would boost the prospects of commodities exporters. Over time, EM bonds have provided investors with differentiated returns relative to DMs, showing modest correlation to global equities and global bonds. The result being ample diversification benefits for institutional investors which can serve as an important buffer during periods of stress or volatility in other regions or asset classes.

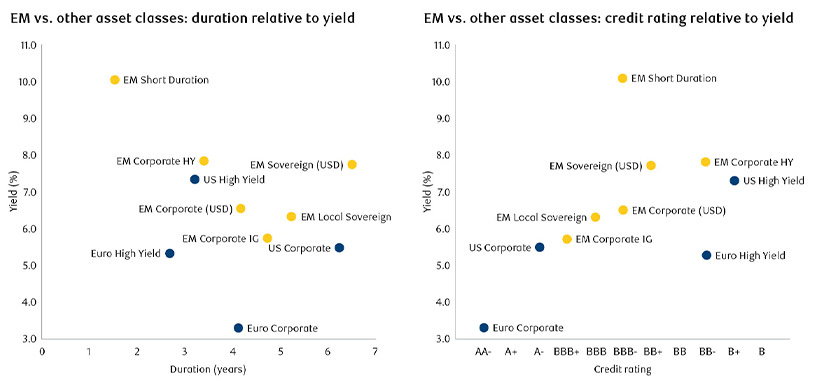

EMD has provided investors with a meaningful yield advantage over developed market bonds, compensating them for venturing out of their core markets and providing an effective cushion against market volatility.

Yields range from 6-7% at the index level and rise to greater than 8% when investors look at instruments rated single-B or below.

This attractive yield premium offered by EMD is apparent when comparing the asset class against developed market instruments with similar rating and duration risk profiles (see Figure 1).

Source: JPMorgan, BofA, Bloomberg. as at 31 January 2025.

Note: EM Corporate (USD) = JPM CEMBI Diversified; EM Sovereign (USD) = JPM EMBI Global Diversified; EM Local Sovereign = JPM GBI-EM Global Diversified USD unhedged; US High Yield = BofA US High Yield Master II; US Corporate = BofA US Corporate Master; Euro High Yield = BofA Euro HY Index; Euro Corporate = BofA Euro Corporate Index; EM Corporate HY = JPM CEMBI Diversified HY, and EM Corporate IG = JPM CEMBI Diversified IG.

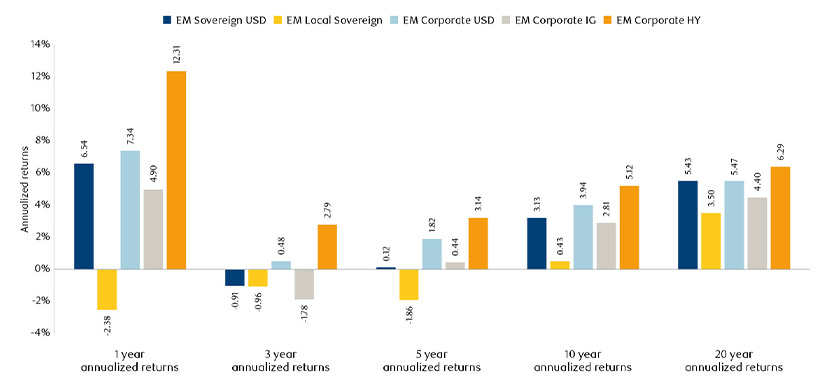

For clients who believe in the benefit of active management they need to look no further than emerging market debt, which provides a fertile a hunting ground for sourcing alpha opportunities. The market can be inefficient and less well understood, as many market participants do not have the resource and expertise to analyse all the risks (and opportunities) and properly price these securities. As a result, specialist active managers can be presented with a ‘dream scenario’, to exploit the price anomaliesthat emerge.

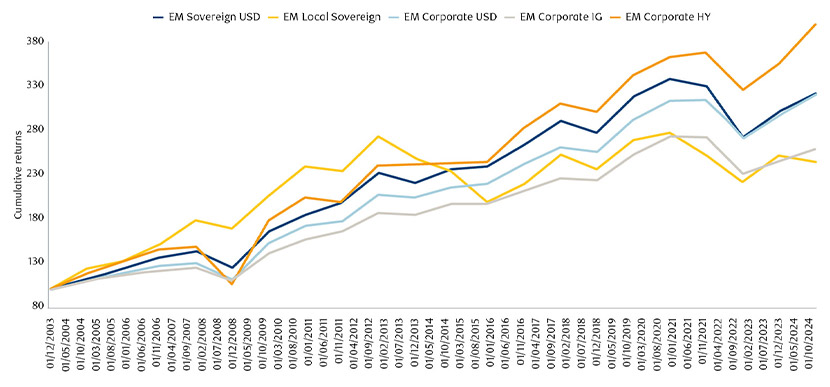

EMs are by their nature subject to swings in sentiment and to external economic and geopolitical events. We believe the wide range of issuers and asset characteristics can create opportunities for enhanced returns through active management as markets overreact in the short term to news flow. The range of exploitable returns can vary across sub-asset classes, depending on the context and market developments. Figures 2 & 3 demonstrate the competitive results achieved by EMD over time.

Source: Bloomberg, as at 31 December 2024

Source: Bloomberg, as at 31 December 2024.

Please choose from the following

We are unable to market if your country is not listed.

You may only access the public pages of our website.