Location

Please select your investor type by clicking on a box:

Terms & conditions

We are unable to market if your country is not listed.

You may only access the public pages of our website.

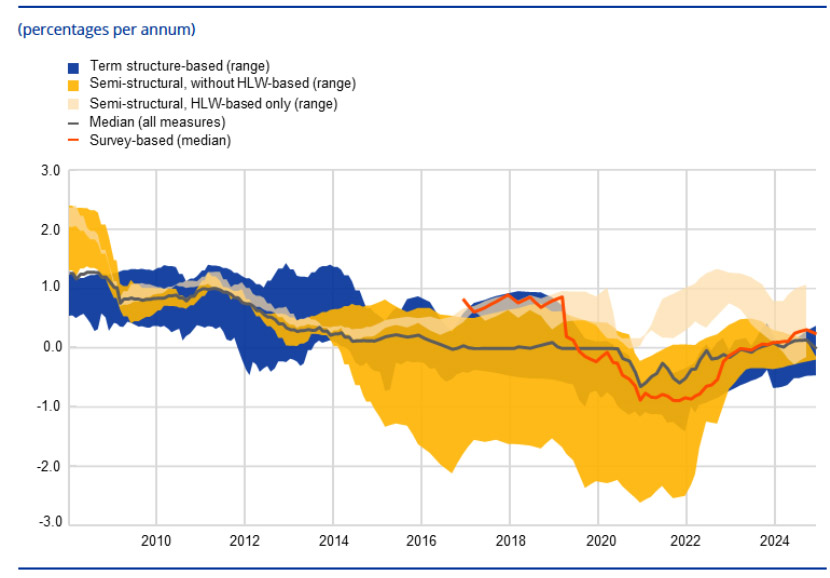

Where we stand: at the last ECB meeting, President Christine Lagarde reinforced the current policy stance, stating that “the disinflationary process is over.” She pointed to resilience in the domestic economy, a strong labour market, and a more balanced risk outlook.

Reality check: yet, any sign of economic softness, particularly on the price front, could embolden the doves to push for further easing.

By the numbers: current estimates of the neutral interest rate (r*) range from 1.75% to 2.25%. ECB staff projections peg inflation at 1.9% by 2027. Wage growth is forecast at 4.6% in 2024 and 3.2% in 2025, based on 47.9% coverage.

The bottom line: another 25bps cut early next year is feasible without straying from a ‘neutral’ policy stance.

Source: ECB, as at September 2025.

Source: ECB, as at September 2025.

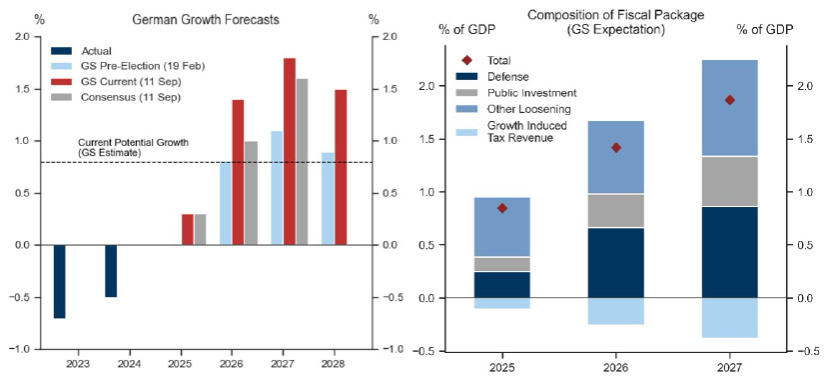

What they’re saying: Goldman Sachs remains optimistic about Germany’s economic prospects, projecting GDP growth roughly 0.5 percentage points above consensus forecasts.

The big picture: political infighting, global trade headwinds, elevated energy costs, and underinvestment in high-tech sectors continue to weigh on momentum. However, the overall trajectory remains upward.

Context: Germany’s rearmament drive is set to deliver significant benefits to European industry. Domestically, efforts to improve supply chains and upgrade infrastructure are poised to enhance long-term growth potential.

What’s next: Europe’s structural transformation is still in its early stages. The first comprehensive audit of the Draghi Report recommendations reveals limited progress: only 11.2% of 383 recommendations have been fully implemented, rising to 31.4% if partial implementations are included. Most remain works in progress.

Source: Goldman Sachs, as at September 2025.

Source: Goldman Sachs, as at September 2025.

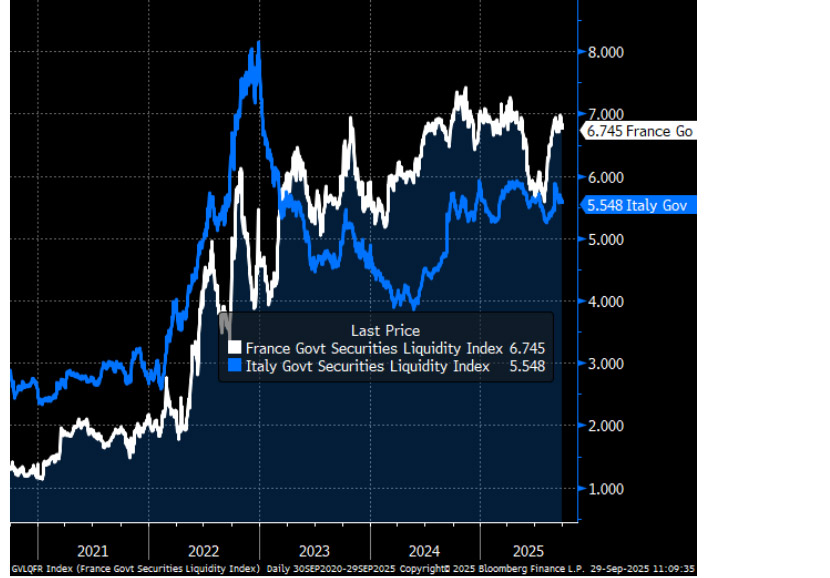

Where we stand: France’s swollen budget deficit, a lingering consequence of the pandemic, highlights successive governments’ failure to rein in spending amid weak economic growth. The new PM faces a daunting task to pass a budget much like his predecessors.

Reality check: political uncertainty and deadlock often triggers markets to price in worst-case scenarios. In such moments, reduced liquidity can amplify the situation, causing spreads to spike sharply in a self-reinforcing cycle.

Why it matters: markets tend to trade against positions, driving spread overshoots. For investors, the best alpha opportunities typically emerge when these trends begin to reverse.

The bottom line: a robust framework for assessing medium- to long-term fair value is essential, offering a reliable anchor for investment decisions during volatile periods.

Source: Bloomberg, as at September 2025.

Source: Bloomberg, as at September 2025.

The big picture: France’s fiscal trajectory has been uniquely idiosyncratic, with bond spreads widening back towards 2024 levels. This contrasts starkly with the broader Eurozone, where government bond spreads have narrowed in recent weeks. Italian 10-year BTPs, once seen as riskier assets, have reached levels not seen since 2008.

Where we stand: the Eurozone periphery, once defined by high debt, soaring unemployment, political instability, and fraught relations with Brussels, has undergone a striking transformation.

Reality check: under Giorgia Meloni, Italy has achieved greater stability and direction. Greece has sharply reduced its debt burden and regained investment grade status. Spain has become one of Europe’s fastest-growing major economies, while Ireland has strengthened its EU ties post-Brexit.

Implications: the traditional core-periphery divide has never been less relevant, with the widest and tightest eurozone sovereign bond spreads now separated by just 60bps.

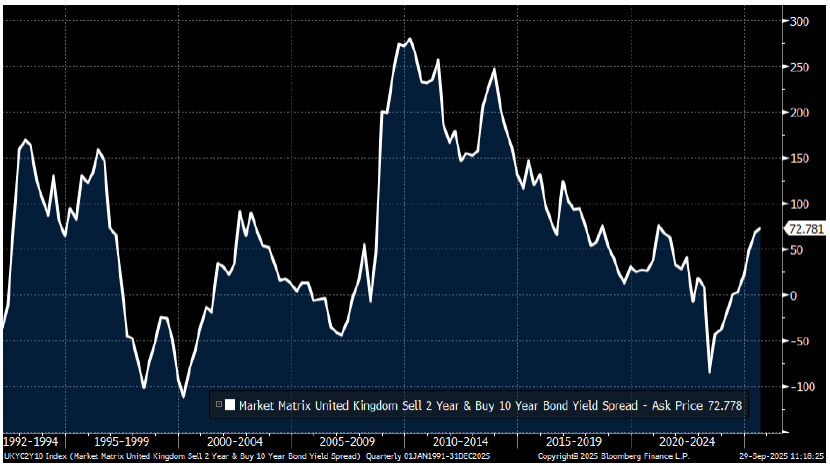

Zoom out: the long end of the gilt market is precariously balanced, with mounting risks from both inflation and government spending.

Reality check: any missteps in controlling inflation or maintaining fiscal discipline could push long-end yields above 6%, steepening the curve dramatically.

Implications: for investors, the short end of the curve may present a safer option. The BoE governor remains adamant the next step remains another cut in policy rates, with one eye on a dubious labour market.

Bottom line: the market is pricing one more additional cut over the next five MPC meetings. As we have seen in the past, these extreme pricing directions don’t last very long.

Source: Bloomberg, as at September 2025.

Source: Bloomberg, as at September 2025.

All data sourced from Bloomberg, as at September 2025, unless otherwise stated.

Please choose from the following

We are unable to market if your country is not listed.

You may only access the public pages of our website.