Location

Please select your investor type by clicking on a box:

Terms & conditions

We are unable to market if your country is not listed.

You may only access the public pages of our website.

Zoom out: the ECB is largely satisfied with its current policy stance, as inflation hovers above 2% and the risk of economic overheating remains low.

By the numbers: markets are pricing in very little in terms of rate cuts over the next four ECB meetings – a mere 8bps.

Where we stand: the ECB is operating in "risk management" mode, meaning any signs of significant downside growth risks could trigger a swift re-pricing in market expectations.

What they’re saying: some policymakers argue that a 2028 inflation projection below 2% – at the December meeting – could justify re-opening rate cut discussions.

The bottom line: it isn’t the base case but should inflation – led by wages – slow further and growth disappoint, don’t be surprised if the rate cut debate heats up again.

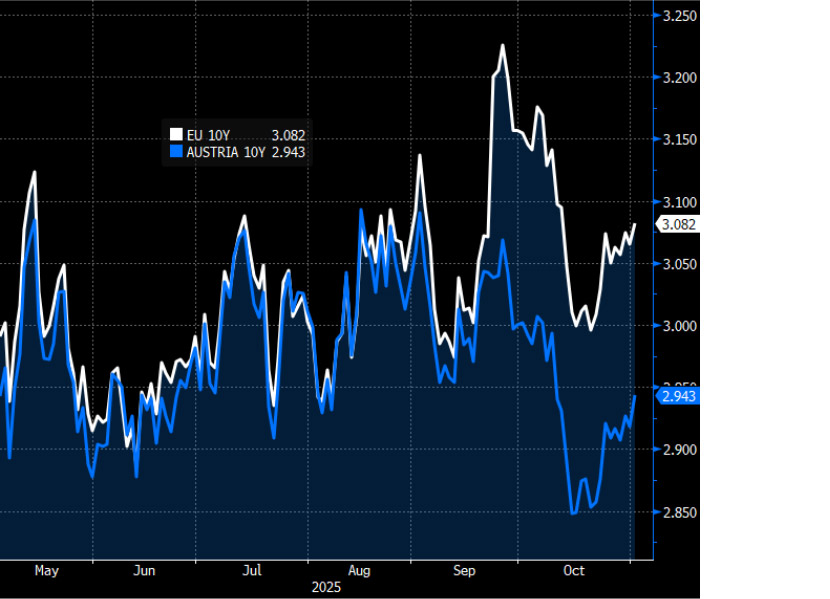

The big picture: the Eurozone’s creditworthiness is improving overall, led by rating upgrades (e.g. Spain, Italy, Greece) outpacing downgrades (e.g. France, Belgium) in recent quarters.

By the numbers: the generic 10-year EU bond trades in the ‘middle of the pack’ versus peers, yielding 3.1%, despite its superior rating.

Context: issuance will remain relatively high, but the launch of the EU bond future is a stepping stone in bolstering liquidity, creating a favourable environment for EU bonds.

What’s next: expect more credit convergence, and in turn, strong supranationals like the EU to converge with the strongest names in the area, such as Austria.

Source: Bloomberg, as at 3 November 2025.

The big picture: Sweden’s economic outlook is improving, with lower rates, rising sentiment, and a shift towards expansionary fiscal policy expected to boost growth.

Zoom in: the Economic Sentiment Indicator (ESI) climbed in October, surpassing normal levels for the first time since mid-2022. Retail confidence is also near historical highs.

Context: Sweden is pivoting away from years of austerity, with fiscal policy in 2026 set to be highly expansionary. JPMorgan estimates a fiscal thrust of 0.7% for 2026, based on budget item multipliers.

The bottom line: Sweden’s policy shift and improving sentiment signal a favourable outlook, positioning the country for stronger growth in 2026, something Riksbank policymakers will be fully aware of.

Source: SEB, as at November 2025.

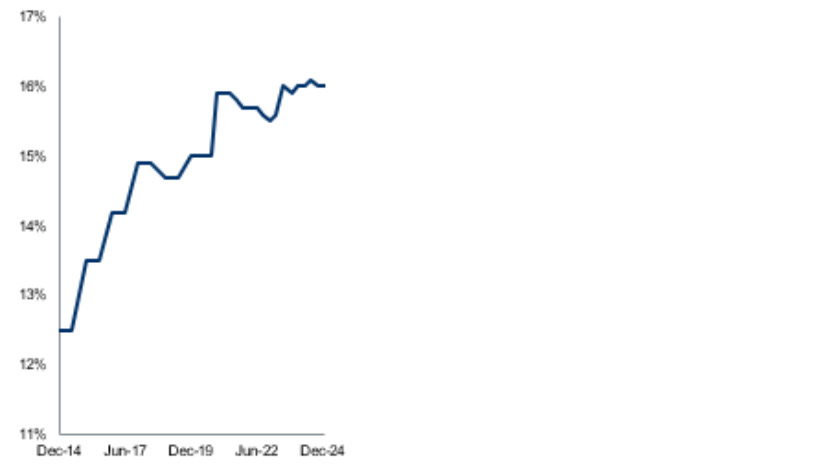

The big picture: cash credit spreads are at multi-year lows, appearing unremarkable on the surface.

Zoom in: while overall spreads may seem unappealing, sectors like European banks with robust fundamentals and improving metrics, offer compelling opportunities for selective positioning.

By the numbers: we have seen CET1 ratios rising from 12.5% in 2014 to 16% today. Return on investment has climbed from 4% to 10%, while non-performing loans have dropped significantly from 6.5% to 2% in the same time period.

Context: the sector has benefited from normalised interest rates, driving a 70% surge in profitability.

The bottom line: investors should look beyond headline spreads to identify resilient sectors, such as European banks, that can deliver strong returns in the current environment.

Source: RBC GAM, as at December 2024.

The big picture: UK 10-year gilts have performed well recently, supported by softer wage and inflation data, alongside government signals of potential energy cost relief.

Context: ongoing "drip-feed" announcements of potential budget policies, including tax hikes for the wealthy, have pressured the pound on concerns they will be detrimental on growth.

Why it matters: the Labour government needs to thread the needle between raising enough money to balance the books and tax hikes that can be digested without any negative growth feedback.

The bottom line: headline inflation has improved, but is still 3.8% (Services is 4.7%), nearly double the Bank of England target. Meanwhile, growth is teetering and needs a boost. The threat of stagflation is there for all to see.

Source: Bloomberg, as at 3 November 2025.

All data sourced from Bloomberg, as at October 2025, unless otherwise stated.

Please choose from the following

We are unable to market if your country is not listed.

You may only access the public pages of our website.