Location

Please select your investor type by clicking on a box:

Terms & conditions

We are unable to market if your country is not listed.

You may only access the public pages of our website.

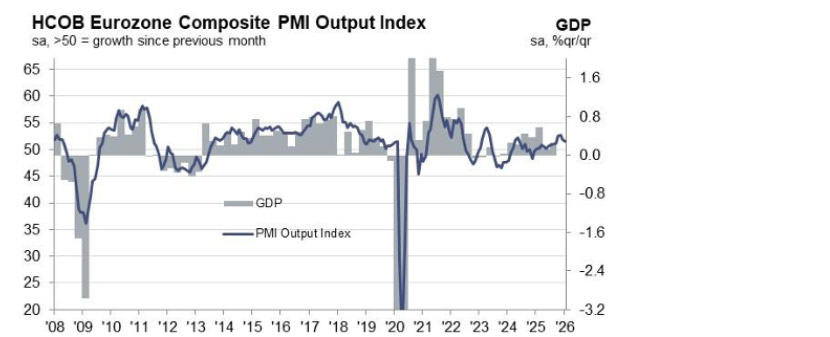

Where we stand: the ECB cut policy rates eight times across 2024-2025. Rates now sit at 2%, widely considered the ‘neutral’ level.

What they're saying: markets are pricing a full 25bps hike by end-2027. Some council members, notably the arch-hawk, Schnabel, are comfortable with that.

Reality check: after the supply-shock induced inflation surge in 2022, many policymakers are paranoid about a repeat scenario.

Big picture: growth is uninspiring (e.g. the latest PMI is just above 50), credit demand is tepid, and Europe is at a critical geopolitical juncture. The ECB can play an important role.

Implications: we think headline inflation will undershoot 2% in H1 2026, allowing the doves at the ECB to become louder.

Source: S&P Global, as at January 2026.

Between the lines: European government bond (EGB) investors have taken note, with further credit spread compression between the strongest and weakest sovereigns in the complex.

By the numbers: there is just a 75bps spread between the Netherlands (strongest) and Lithuania (weakest). This was as wide as 150bps in early 2025.

Bonus: despite longer-term political and fiscal problems, noise around France has dissipated after the passing of the budget (until 2027 at least).

Bottom line: the reach for yield has been fierce in 2026. The need for Europeans to be united in a fractious international environment has provided a tailwind for narrowing credit spreads in the EGB space.

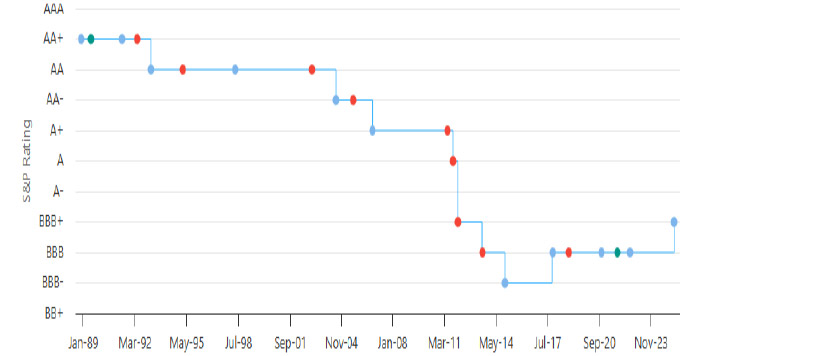

Where we stand: Italy is on a roll; a successful syndication earlier this month attracted orders exceeding EUR150 billion and recent investor meetings were notably upbeat.

Zoom out: political stability has proved highly beneficial, as have efforts to consolidate debt. The government expects positive primary balances of 1.2% in 2026, rising to 1.9% by 2029.

Zoom in: Italy has emerged as one of the market's preferred sovereign borrowers, with a broadening regional investor base, most notably from the Nordics and the Middle East.

Bottom line: Italy has a diverse mix of investors, including a strong retail presence. As the ECB steps away, international investors are happy to fill the gap.

Source: Highcharts.com, as at January 2026.

Zoom out: last summer, ECB vice president de Guindos said a EURUSD level above 1.20 would be ‘complicated’.

What they’re saying: 2026 has started with 1.20 under pressure. Other ECB members such as Villeroy and Kocher have already spoken out, highlighting the potential impact on inflation and the readiness to act.

Reality check: the trust in US policymaking is largely the narrative, accelerated recently by speculation around joint US-Japanese FX intervention. The truth is, euro trade-weighted has barely budged.

Why it matters: higher EURUSD feeds into costlier exports. According to GS, the largest European publicly listed companies derive 30% of their revenues from the US.

Bottom line: if the euro continues its ascent versus the US dollar, more ECB heads will turn.

Source: Bloomberg, as at January 2026.

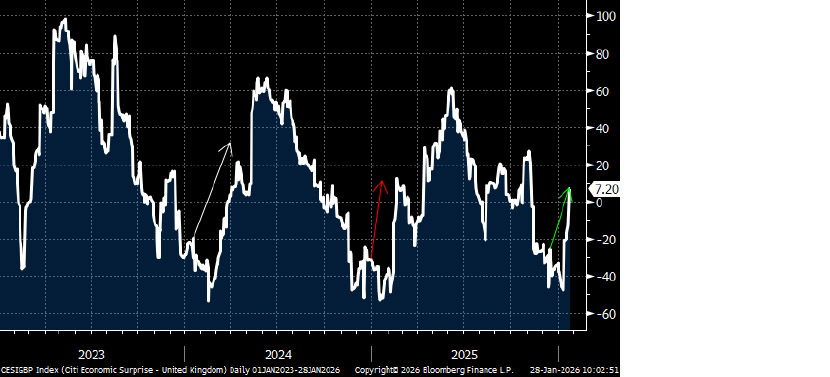

Where we stand: GDP, retail sales, and PMI data in January beat market expectations, confounding the generally bearish views of the UK economy.

Context: however, you could argue the strength is rather seasonal, given recent history, in which the UK economy starts the year strongly.

Reality check: the jobs market remains sluggish, with the latest unemployment rate holding above 5% and youth unemployment continuing to rise.

What’s next: the government remains entangled with geopolitics, domestic policy U-turns, and infighting. To make matters worse, inflationary pressures have stalled somewhat, according to the BRC.

Implications: the pound has moved sideways (versus the EUR) so far this year, but if growth tails off as the year moves on, and inflation remains stickier than expected, ‘the quid’ will have no choice but to bear the brunt.

Source: Bloomberg, as at January 2026.

All data sourced from Bloomberg, as at January 2026, unless otherwise stated.

Please choose from the following

We are unable to market if your country is not listed.

You may only access the public pages of our website.