Location

Please select your investor type by clicking on a box:

We are unable to market if your country is not listed.

You may only access the public pages of our website.

Key takeaways

Tariff uncertainty collided with post-election optimism earlier this year. De-regulatory supply-side policies have a deflationary bias considered positive for corporate profits. Tariffs, on the other hand, have to be paid for, pushing up prices and disrupting supply chains. Fears of recession increased, creating ‘push’ factors for capital to leave the U.S.. This is in contrast to Europe where security fears encouraged governments to prioritise rearmament spending at the same time as interest rates continued to be cut.

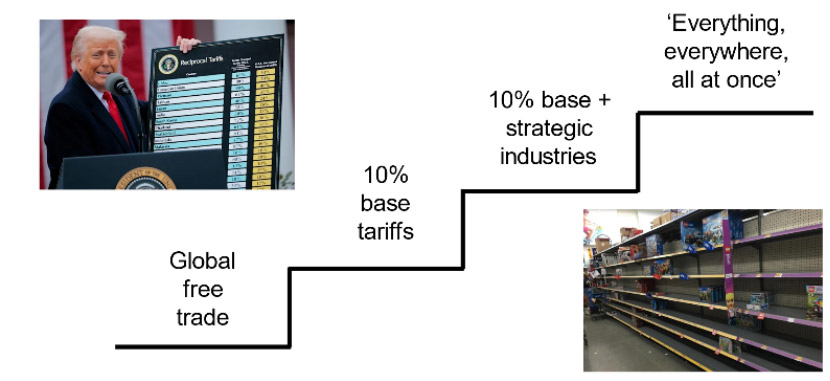

Investors and companies still don’t have the tariff policy certainty they crave. Different voices argue for different outcomes, creating a ‘stairway to liberation’ of compounding policy actions.

The tariff ‘stairway to liberation’

The first step, a 10% tariff on all imports, would be frustrating for companies, investors and consumers. But it would likely not force companies to rapidly change supply chains and would raise significant revenue for government coffers.

Some argue it doesn’t go far enough. The next step builds on the first by adding in tariffs on strategic industries, like rare earths, semiconductors and pharmaceuticals to encourage domestic re-shoring and support U.S. economic security. This is a more interventionist approach but if limited to specific business models, it is one that the market should be able to price effectively.

The final step is essentially the full ‘Rose Garden’ treatment with reciprocal tariffs based upon existing trade deficits, in particular with China, with the goal of reindustrialisation. This last step was quickly priced into equity markets after the ‘Rose Garden’ announcement elevated the risk of recession.

The 90-day moratorium on new tariffs came as a significant relief to equity markets. The implicit signal was that the risk of ‘everything, everywhere, all at once’ is significantly reduced. It was a well-timed intervention. Orders for Halloween and Christmas retail inventory need to be placed around now if product is to arrive in time, with delays risking empty shelves at Walmart. President Trump doesn’t want to be the President who cancelled Christmas.

Market consensus has moved back down the stairway and now appears to be somewhere between steps 1 and 2.

This is a better outcome than feared in early April that has helped equity markets recover their early Spring losses. The implied risk of recession has fallen from above 50% to somewhere in the 30s% (compared to a notional probability of 20-25% in any given year).

There are a few things we don’t yet know. Firstly, will there be a long-lasting trade agreement between the U.S. and China? Scott Bessent, Treasury Secretary, has said that neither country wants to ‘decouple’ from the other, which if true may indicate a settlement is possible. But this is in conflict with the re-industrialisation objective that requires a degree of inevitable decoupling, so who is right?

Secondly, even if outline deals are agreed in the next 60 days, will they be strong enough to give companies the confidence to invest? Or will delays cause an activity air-pocket and push the U.S. into recession anyway?

Finally, might we be looking at stagflation (lower growth and inflation above 2% for longer) or a ‘Goldilocks’ economy (3% growth and inflation 2-3%) in future? The market is looking for clues, hence the focus on ‘soft’ (current survey data) and ‘hard’ (backward-looking official data) economic indicators. Results so far are somewhat ambiguous.

So far, companies’ reported Q1 earnings have been better than feared. But Q1 was arguably always a ‘pass’ given that tariffs weren’t fully announced until the beginning of Q2. Earnings estimates have held up surprisingly well, despite ongoing policy uncertainty, but profit estimates often fade through the second half. Given valuations have recovered, this is leading many investors to ask ‘now what?’

The market rotation from the U.S. to Europe feels as though it has stalled. Tech stocks and ‘retail favourites’, such as Tesla, have been doing better lately. It is probably dangerous to be too dismissive of the U.S.. The natural advantages the country has in terms of its innovation-friendly eco-system, expanding demographics and high labour productivity all still mean that anyone looking to allocate their marginal dollar will have to consider the U.S. economy. The popularity of passive investment solutions in the U.S. also continues to act as a magnet for global capital as firms look to list in a market where passive means there is a surfeit of wealthy, value-agnostic investors.

In contrast, Europe has potential, but we have yet to see sustained commitment to the type of economic reforms and liberalisation that were set out in Mario Draghi’s 2024 report. A re-ordering of spending priorities in favour of defence is making new funds available which, together with falling interest rates, is supporting hopes of an improved environment to corporate profitability. However, this is a simple transient multiplier effect to growth – sustained economic growth probably requires supply-side reforms, the appetite for which remains unclear. A useful test-case for investors to monitor is cross-border banking consolidation, such as UniCredit’s approach to Commerzbank.

Our approach is a focus on company fundamentals, especially quality companies run by strong management teams, as they will be more resilient and will likely be able to take advantage of industry change better than weaker competitors. It is also important not to forget risk. Recent market volatility has highlighted the dangers of taking a strong market (beta) or country (U.S. versus Europe) view. Better to diversify such macro risks, monitor positive momentum exposure by not letting position sizes drift too far and let the company holdings do the talking.

Source: Bloomberg or publicly available data, as at May 2025.

Erhalten Sie jetzt aktuelle Investment- und Wirtschaftsanalysen unserer Experten direkt in Ihre Mailbox.

Bei diesem Dokument handelt es sich um eine Marketingmitteilung, die von folgenden Stellen erstellt und herausgegeben werden kann: im Europäischen Wirtschaftsraum (EWR) von BlueBay Funds Management Company S.A. (BBFM S.A.), die von der Commission de Surveillance du Secteur Financier (CSSF) reguliert wird. In Deutschland, Italien, Spanien und den Niederlanden ist die BBFM S.A. im Rahmen einer Zweigniederlassungsgenehmigung gemäss der Richtlinie über Organismen für gemeinsame Anlagen in Wertpapieren (2009/65/EG) und der Richtlinie über die Verwalter alternativer Investmentfonds (2011/61/EU) tätig. Im Vereinigten Königreich (UK) durch RBC Global Asset Management (UK) Limited (RBC GAM UK), die von der britischen Financial Conduct Authority (FCA) zugelassen und beaufsichtigt wird, bei der US Securities and Exchange Commission (SEC) registriert ist und Mitglied der National Futures Association (NFA) ist, die von der US Commodity Futures Trading Commission (CFTC) zugelassen ist. In der Schweiz durch die BlueBay Asset Management AG, deren Vertreter und Zahlstelle die BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zürich, Schweiz ist. Der Erfüllungsort befindet sich am Sitz des Vertreters. Für Klagen im Zusammenhang mit dem Angebot und/oder der Bewerbung von Aktien in der Schweiz sind die Gerichte am Sitz des schweizerischen Vertreters oder am Sitz oder Wohnsitz des Anlegers zuständig. Der Prospekt, die wesentlichen Anlegerinformationen (Key Investor Information Documents - KIIDs), die wesentlichen Informationen über Anlageprodukte für Kleinanleger und Versicherungsprodukte (Packaged Retail and Insurance-based Investment Products - Key Information Documents - PRIIPs KIDs), soweit zutreffend, die Satzung und alle anderen erforderlichen Dokumente, wie z.B. die Jahres- und Halbjahresberichte, können kostenlos beim Vertreter in der Schweiz bezogen werden. In Japan durch BlueBay Asset Management International Limited, die beim Kanto Local Finance Bureau des japanischen Finanzministeriums registriert ist. In Asien durch RBC Global Asset Management (Asia) Limited, die bei der Securities and Futures Commission (SFC) in Hongkong registriert ist. In Australien ist RBC GAM UK von dem Erfordernis einer australischen Finanzdienstleistungslizenz gemäss dem Corporations Act befreit, da sie von der FCA nach den Gesetzen des Vereinigten Königreichs reguliert wird, die sich von den australischen Gesetzen unterscheiden. In Kanada durch RBC Global Asset Management Inc. (einschließlich PH&N Institutional), die der Aufsicht der Wertpapieraufsichtsbehörde der jeweiligen Provinz bzw. des Territoriums unterliegt, bei der sie registriert ist. RBC GAM UK ist nicht nach den Wertpapiergesetzen registriert und beruft sich auf die Ausnahmeregelung für internationale Händler nach den geltenden Wertpapiergesetzen der Provinzen, die es RBC GAM UK erlaubt, bestimmte spezifizierte Händlertätigkeiten für in Kanada ansässige Personen auszuüben, die als "zugelassener kanadischer Kunde" im Sinne der geltenden Wertpapiergesetze gelten. In den Vereinigten Staaten durch RBC Global Asset Management (U.S.) Inc. („RBC GAM-US“), einen bei der SEC registrierten Anlageberater. Die oben genannten Unternehmen werden in diesem Dokument gemeinsam als „RBC BlueBay“ bezeichnet. Die angegebenen Registrierungen und Mitgliedschaften sind nicht als Befürwortung oder Genehmigung von RBC BlueBay durch die jeweiligen lizenzierenden oder registrierenden Behörden auszulegen. Nicht alle hierin beschriebenen Produkte, Dienstleistungen oder Anlagen sind in allen Rechtsordnungen verfügbar, und einige sind aufgrund lokaler aufsichtsrechtlicher und rechtlicher Anforderungen nur eingeschränkt verfügbar.

Dieses Dokument ist nur für „Professionelle Kunden“ und „Geeignete Gegenparteien“ (im Sinne der Richtlinie über Märkte für Finanzinstrumente („MiFID“) oder der FCA) oder in der Schweiz für „Qualifizierte Anleger“ im Sinne von Artikel 10 des Schweizerischen Kollektivanlagengesetzes und seiner Ausführungsverordnung oder in den USA für „Zugelassene Anleger“ (im Sinne des Securities Act von 1933) oder „Qualifizierte Käufer“ (im Sinne des Investment Company Act von 1940) bestimmt und sollte von keiner anderen Kundenkategorie als verlässlich angesehen werden.

Sofern nicht anders angegeben, wurden alle Daten von RBC BlueBay bezogen. Dieses Dokument ist nach bestem Wissen und Gewissen von RBC BlueBay zum Zeitpunkt der Erstellung wahr und korrekt. RBC BlueBay gibt keine ausdrücklichen oder stillschweigenden Garantien oder Zusicherungen in Bezug auf die in diesem Dokument enthaltenen Informationen und lehnt hiermit ausdrücklich alle Garantien in Bezug auf Genauigkeit, Vollständigkeit oder Eignung für einen bestimmten Zweck ab. Meinungen und Schätzungen stellen unser Urteil dar und können ohne vorherige Ankündigung geändert werden. RBC BlueBay bietet keine Anlage- oder sonstige Beratung an, und nichts in diesem Dokument stellt eine Beratung dar und sollte auch nicht als solche interpretiert werden. Dieses Dokument stellt weder ein Angebot zum Verkauf noch eine Aufforderung zum Kauf von Wertpapieren oder Anlageprodukten in irgendeiner Rechtsordnung dar und dient ausschliesslich Informationszwecken.

Kein Teil dieses Dokuments darf zu irgendeinem Zweck oder auf irgendeine Art ohne die vorherige, schriftliche Einwilligung von RBC BlueBay reproduziert, weiterverteilt, direkt oder indirekt an irgendeine andere Person übermittelt bzw. ganz oder auszugsweise veröffentlicht werden. Copyright 2023 © RBC BlueBay. RBC Global Asset Management (RBC GAM) ist die Vermögensverwaltungsdivision der Royal Bank of Canada (RBC), zu der die RBC Global Asset Management (U.S.) Inc. (RBC GAM-US), RBC Global Asset Management Inc., RBC Global Asset Management (UK) Limited und RBC Global Asset Management (Asia) Limited gehören, bei denen es sich um separate, aber verbundene Unternehmen handelt. ® / Eingetragene Marke(n) der Royal Bank of Canada und BlueBay Asset Management (Services) Ltd. Verwendet unter Lizenz. BlueBay Funds Management Company S.A., eingetragener Sitz 4, Boulevard Royal L-2449 Luxemburg, in Luxemburg unter der Nummer B88445 eingetragene Gesellschaft. RBC Global Asset Management (UK) Limited, eingetragener Firmensitz 100 Bishopsgate, London EC2N 4AA, eingetragen in England und Wales unter der Nummer 03647343. Alle Rechte vorbehalten

Erhalten Sie jetzt aktuelle Investment- und Wirtschaftsanalysen unserer Experten direkt in Ihre Mailbox.

Please choose from the following

We are unable to market if your country is not listed.

You may only access the public pages of our website.